In 1969, Creedence Clearwater Revival released what would become one of the defining songs of a generation.

Source: SoundCloud

"Fortunate Son" was John Fogerty's protest against a system that seemed to ask more of some young Americans than others. While working-class kids were disproportionately sent to Vietnam, the sons of wealthy and politically connected families often found ways to avoid the consequences.

If you are not familiar with this song or would just like to hear it again, I have included a YouTube link below with lyrics for your listening pleasure.

Creedence Clearwater Revival - Fortunate Son

The song was not really about war. It was about privilege. More specifically, it was about how who your parents were could shape your opportunities in life.

More than fifty years later, America has its own version of the fortunate son. Or perhaps more accurately, the fortunate son or daughter.

They are not avoiding the draft. They are navigating the affordability crisis. And their parents may be helping more than most economists realize.

One of the great mysteries of the current economy is why the American consumer refuses to crack. Economic headlines routinely point to slowing income growth, softening wage gains, and signs of financial strain. Yet consumer spending remains surprisingly resilient. Retail sales continue to hold up. Travel spending remains strong. Restaurants remain busy. The economy continues to grow.

For two years, economists have been asking a simple question. How can consumption remain so strong when income data appears so weak?

Dr. Ed Yardeni, who is one of the economists and market strategists that our Investylitics committee follows, believes economists are looking in the wrong place.

At this year's Mauldin Economics Strategic Investment Conference, Ed offered what I believe is one of the most compelling explanations for this puzzle. He calls it the G-shaped economy.

The G stands for generational. And that single letter may explain one of the biggest economic puzzles of the past two years.

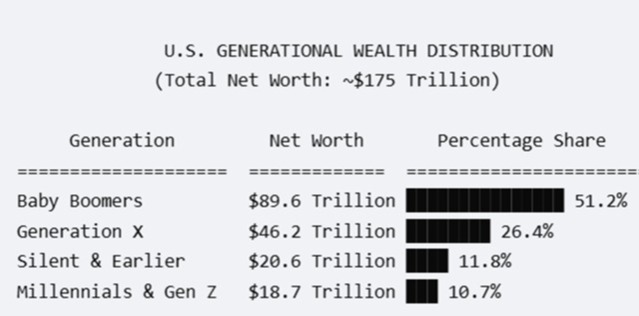

According to Federal Reserve data, baby boomers collectively control approximately $89 trillion in net worth, as you can see in our first chart below.

Source: Federal Reserve Bank, Investopedia

The Federal Reserve's generational wealth data confirm that the Baby Boomer generation holds $89.6 trillion in net worth, accounting for 51.2% of all household wealth in the United States.

Boomer wealth is concentrated in stocks, mutual funds, retirement accounts, and home equity, the very assets that have experienced extraordinary appreciation over the last four decades. As a generation, they benefited from decades of rising home values, rising stock prices, pension accumulation, and one of the greatest periods of wealth creation in American history.

At the same time, they are retiring in record numbers. In 2025 alone, approximately 1.85 million retired workers filed for Social Security benefits for the first time.

When someone retires, their paycheck disappears.

But their wealth does not. That distinction matters.

As boomers leave the workforce, they stop contributing wage income that shows up in government statistics. Disposable income growth slows. Average hourly earnings weaken. The economic data begins to suggest a softer consumer.

Yet many retirees continue to spend because they are drawing on accumulated wealth rather than a paycheck.

Retirement removes income from the statistics. It does not remove purchasing power from the economy. That is where the story becomes even more interesting.

When I turned 21, most of my friends and I couldn't wait to get out of the house and live on our own. My wife Rachel started living on her own just before her 18th birthday, when she graduated from high school. Her mom took a job in Arizona while she stayed in Georgia and got a job to pay for her rent and car. Today, that experience is becoming increasingly rare.

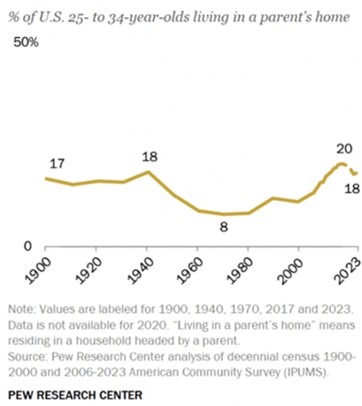

Recent data shows that nearly one in five adults between the ages of 25 and 34 now live with a parent. That number has doubled since 1980, as you can see in our next chart below, and is back to levels not seen since before World War II, in the latter stages of the Great Depression.

Source: Pew Research Center

Some do so by choice, but many are doing so because housing affordability has become increasingly difficult. Others receive help with rent, childcare, tuition payments, down payments, insurance costs, or everyday living expenses.

The affordability crisis facing younger Americans is real. So is the financial support flowing from older generations.

Last year, I wrote about America's K-shaped economy. The upper branch of the K represented households benefiting from rising asset values and growing wealth. The lower branch represented those struggling with affordability, stagnant purchasing power, and limited asset ownership. A link to that article is included below if you would like to revisit it.

https://www.impelwealth.com/blog/our-challenging-special-k-economy

The K-shaped economy explains the divide.

The G-shaped economy explains the bridge.

In many ways, the G-shaped economy is helping soften the consequences of the K-shaped economy.

The wealth accumulated by older generations is increasingly supporting spending by younger generations. Parents and grandparents are helping children and grandchildren navigate a more expensive world. That support may not show up as earned income, but it certainly shows up in spending.

I can tell you from firsthand experience, it shows up in conversations I have with clients almost weekly. Many of my clients who have accumulated more than they are likely to spend in retirement are actively looking for ways to share those resources with children and grandchildren today rather than waiting for an eventual inheritance.

When a 28-year-old lives rent-free in a parent's home, the parent's balance sheet effectively becomes part of the child's income statement. When grandparents contribute to a 529 plan, help fund a down payment, or cover childcare expenses, the result is additional spending power that traditional economic measures often fail to capture.

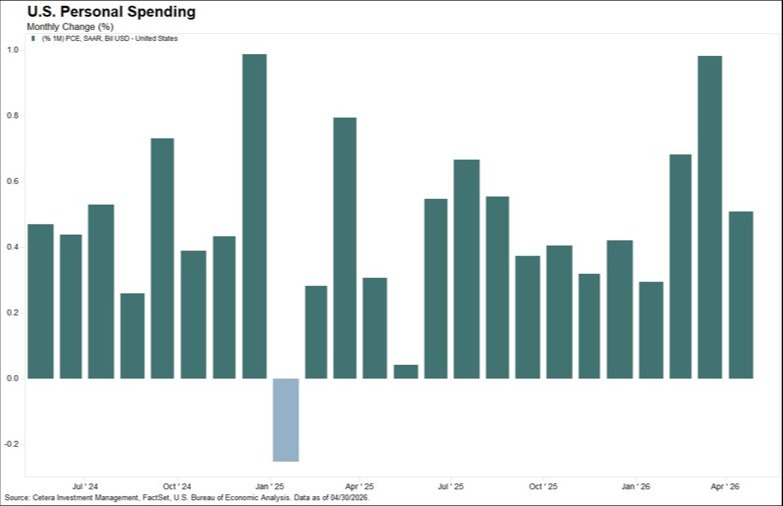

The money does not disappear. It gets spent. It simply changes hands. This may explain why consumption has consistently exceeded what many economists expected based solely on income data, as shown in our final chart below.

Traditional economic models were built around a simple relationship: income drives consumption. Increasingly, however, America appears to be operating under a different equation.

Assets drive transfers. Transfers drive consumption.

The distinction is important because economists are generally very good at measuring income and far less effective at measuring the economic impact of wealth transfers occurring within families.

The bears have spent the last two years pointing to weakening income growth as evidence that the consumer is about to run out of steam. They may eventually be right. But they may be underestimating the role accumulated wealth plays today.

The story does not end with today's spending patterns. It might only be the beginning.

This $89 trillion peak in Baby Boomer wealth is the foundation for the "Great Wealth Transfer", in which an estimated $84 trillion is projected to pass to Gen X, Millennial, and Gen Z heirs over the next two decades.

This has important implications for investors and financial planning.

For investors, it suggests that consumer spending may remain stronger than traditional income measures imply. Wealth effects may be more important than wage growth in explaining economic activity. Demographics may matter more than many market forecasts currently assume.

For financial planning, it highlights a reality many families are already experiencing firsthand. The "Great Wealth Transfer" is no longer a future event.

For many families, it is becoming a living event rather than a legacy event. And, it is happening now.

Many of my retired clients are not waiting to pass wealth to the next generation through an estate. They are helping children and grandchildren while they are alive. Part of this is knowing, from the financial planning process, that they have surplus assets and do not have to wait until they pass away to leave a large inheritance to their children and grandchildren.

However, in conversations happening in my office today, clients are telling me they want to be around to see their children and grandchildren benefit from the surplus resources they have accumulated. Part of the joy of giving to the next generation is being there to see how they benefit from these intergenerational wealth transfers.

They don't just want to leave a legacy. They want to experience it.

They are funding education, helping with housing, assisting with childcare, and providing the financial support necessary to navigate an increasingly expensive economy. We love helping clients build the confidence they need to begin their journey of gifting and generosity.

Whether that support takes the form of gifts, trusts, 529 plans, or simply opening the door to the family home, the result is the same. The balance sheet of one generation becomes the spending power of another.

That does not mean the system is permanent. Boomers will not be here forever. Wealth eventually gets spent, transferred, or divided among heirs. At some point, the fuel powering this intergenerational support will diminish.

But that day may be further away than the income statistics suggest.

John Fogerty's fortunate sons benefited from who their parents were. Today's fortunate sons and daughters may benefit from something entirely different.

Not political connections. Not special treatment. Simply put, parents and grandparents who spent decades building wealth are now helping the next generation navigate an economy that has become increasingly unaffordable.

That may not show up in the income data. But it certainly shows up at the cash register.

Perhaps Ed Yardeni is right. Perhaps the reason the consumer has remained so resilient is not because economists have misread income. Perhaps they have underestimated the power of accumulated wealth.

The K-shaped economy explains who has benefited from the last several decades of asset appreciation. The G-shaped economy explains how some of that wealth is now flowing to the next generation.

And if that is true, today's fortunate son or daughter may not be the one with the highest income. It may simply be the one with parents or grandparents willing and able to help them keep “Moving Life Forward.”

© 2026 Jesse Hurst

Senior Wealth Manager

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/claffra