In 1995, Steve Luckenbach, a newly hired regional sales manager for one of our product partners, came to my office to tell me how their products could help my clients solve some of their financial needs. It turns out that this was the first call of his sales career. Steve became a good friend and a trusted advisor. He was also a deep thinker who desired to help clients build wealth by managing their beliefs and behaviors. He became an expert in a field of study known as behavioral finance or neuroeconomics that explores how and why people make certain financial decisions and often financial mistakes.

Source: LinkedIn

Steve was passionate about helping people overcome their natural behavioral anchors and biases so they could avoid the mistakes that most people make on their journey to build wealth. Steve, the grandson of a Pentecostal preacher, was also a dynamic speaker. As a matter of fact, Steve was one of the only product partners that I ever invited to share the stage with me. If you have been a client of mine for more than 20 years, you have likely heard him speak at one of our educational events. Steve and I shared the stage several times, including in 2009, a few months after the 2008 AIG and Lehman Brothers meltdown. At the time, many people were questioning whether they should stay invested after the stock market had dropped more than 50%. As the S&P 500 bottomed below 700 on March 9th of that year and today trades hands at above 6000, that was the buying opportunity of a lifetime. However, few people could see past their fears or emotions to take advantage of this.

Source: Amazon.com

In January 2010, Steve released his book Don’t Believe Everything You Think. The book was created to help financial advisors better guide their clients to successful outcomes. It tells the story of three financial professionals' journey through a parable led by a mysterious Guru who shares the secrets to finding wealth, passion, and meaning in their work. Through creative and challenging lessons, they discover the neurological reasons we all make the wrong investment choices. These tend to be driven by external stimuli, such as news and events, and internal beliefs and biases developed throughout your lifetime.

Today, many investors are once again making assumptions or decisions about their financial and investment futures based on a recent event: the outcome of the 2024 election. This is not uncommon. This phenomenon occurs after each election cycle as economists and investment prognosticators try to read the tea leaves of the most recent election to determine who the winners and losers will be. As you will see below, these predictions are oftentimes more wrong than right.

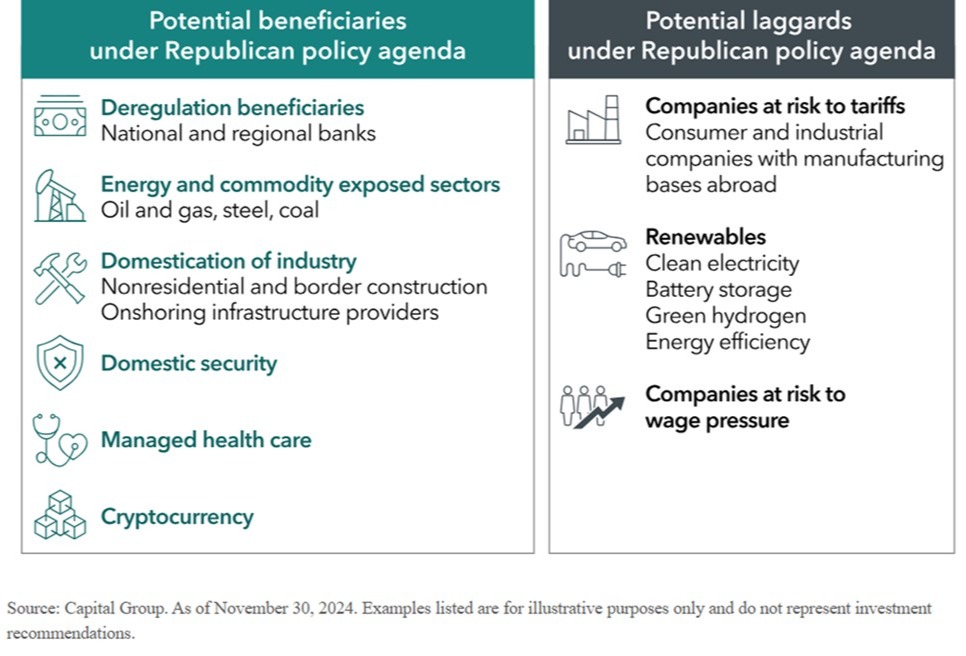

Let's begin by examining a typical example of an investment company trying to tell us what companies or industries may do better or worse under the new administration. The chart below comes from our friends at Capital Group, the American funds. However, I could show you similar charts from many different companies. They all draw on similar themes and concerns.

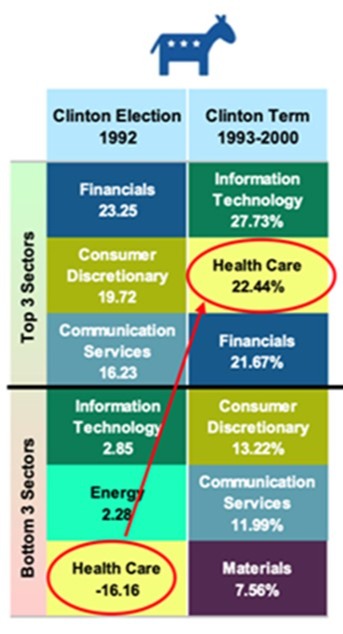

Now, let's look back at history and see how some of these predictions played out in real life. We will start with predictions about healthcare stocks in the wake of President Bill Clinton's election in 1992. You may remember that in 1993, shortly after being elected, the president asked First Lady Hillary Clinton to chair the Task Force on National Health Care Reform. Many market prognosticators assumed that the recommendations and policies from this task force would have a negative impact on healthcare stocks. They advised investors to reduce their holdings of these stocks so that this political process would not hurt their portfolios. How did those recommendations turn out?

When you look at the performance of healthcare stocks during President Bill Clinton's tenure, the recommendation to reduce one's holdings of these stocks seemed like a good idea… for about a year. During his first year in office, these stocks were the bottom-performing sector and lost more than 16%. However, over the ensuing seven years, they were the second-best performing sector, returning more than 22% a year for the balance of his term.

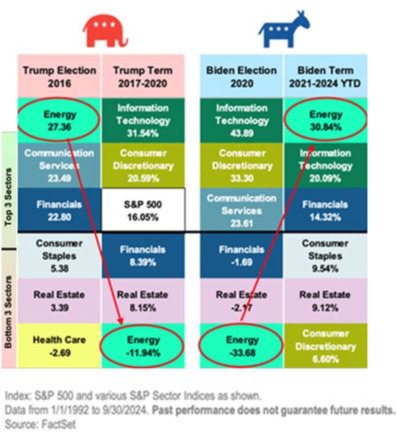

Let's look at two more recent examples and show the results of energy companies in the wake of the 2016 and 2020 elections. Many people will not be surprised to see that energy companies did very well in the wake of the 2016 election. President Trump was, and continues to be, pro-drilling and energy independence. However, many people would be surprised to see how poorly these same energy company stocks did during the balance of his first presidency.

On the flip side, when President Biden was campaigning, he said many times that he would do his best to eliminate the need for oil and gas as quickly as possible. Predictably, when he was elected, energy stocks had an awful 2020. However, this was also because COVID shutdowns meant that people were not flying or driving in many places, and this reduction of demand hurt energy company profits. What is much more surprising is to see how well energy and companies have performed over the last three years under the Biden administration. In fact, they were the top-performing sector, returning more than 30% a year.

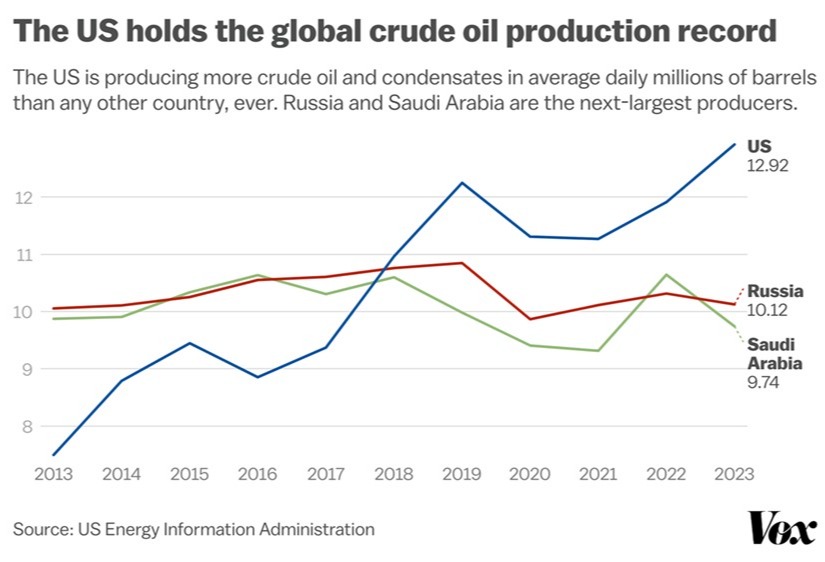

Why did this happen? Great question. As we look at our final graph below, you will see that despite the federal drilling bans put in place by the current administration, continued technological advances in drilling and oil extraction led to the United States producing more oil and gas than it ever has before. In fact, we are now the world's top oil and gas producer, far exceeding the production of Russia and Saudi Arabia.

This is why we shouldn’t believe everything we think, hear, or read. We likely do not know what sector or stocks will do the best in the upcoming administration. This is especially true when there is potential massive change coming in areas such as tax policy, deregulation, immigration, and perhaps most importantly, government spending. There will likely be intended and unintended consequences of these policies, as they typically have been in the past.

What is the best solution for dealing with these unknowns and uncertainty? Rely on tried-and-true investment principles, such as maintaining a disciplined diversification, which is age and risk-profile-appropriate, and rebalancing your portfolio regularly to take advantage of the inevitable ups and downs in the market. The CFPs of Impel Wealth Management will continue to guide you, our trusted friends, and clients during such times. It is our mission and what drives us as we continue “Moving Life Forward.”

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image: iStock.com/azatvaleev