Honey, I Shrunk the Kids is a comic science fiction film, which was released in June 1989. It became a much bigger success than initially expected, grossing $222 million worldwide. Not surprisingly, this success led Disney to put out multiple sequels, a television series, and an EPCOT theme park attraction.

Source: Disney Movies

The 1992 sequel, Honey I Blew Up the Kid, inverted the problem of the first movie, in which scientist, Wayne Szalinski’s children are accidentally shrunk by the inventor's ray gun machine. In the sequel, the youngest son, Adam is accidentally exposed to Wayne‘s new industrial-sized growth machine, which causes him to grow to an enormous size.

In much the same way, the actions of the Federal Reserve Bank, with pandemic stimulus assistance from the federal government, have created policies that have caused monthly mortgage payments to BLOW UP to amounts that are making housing unaffordable to many, especially young families.

The average mortgage interest rate for all of 2021 was 2.96%. By the way, anyone who purchased a home between 2012-2021, was most likely able to lock in a mortgage at 4% or less. In just a little more than two years, mortgage rates have climbed to approximately 7.5% or higher, the highest in more than two decades.

At the same time, housing prices have risen dramatically since the onset of the Covid-19 pandemic. From January 2020 to June 2022, housing prices increased 40% or more nationally. This was partially driven by a flight of people moving from inner cities, where they were locked down in smaller places, to the suburbs where they would have more space for their families. This was given a giant assist by mortgage rates that fell to below 3% in 2021. In fact, the Federal Reserve Bank continued to leave interest rates near 0% as inflation was starting to rise due to pandemic-related fiscal and monetary stimulus.

Most people thought that housing prices would start to cool when the Fed started raising interest rates. This is what happened when the housing bubble burst in 2006. The Fed had been raising interest rates for two years prior to this and eventually, home prices declined for 32 straight months, falling 27% nationally when housing prices finally bottomed in 2012. This also led to nearly 3.8 million homes being lost to foreclosure from 2007 to 2010.

We must remember that housing prices are driven by supply and demand. As there were massive amounts of both speculative building and lending leading to the housing bubble, there was a glut of homes on the market when the downturn hit. This led the housing prices falling in the aftermath of the subprime mortgage bubble bursting.

However, in a post-Covid economy, there has been a severe lack of inventory in the housing market nationally. Most people who have a home with a mortgage under 4%, are not in a hurry to sell and take on a new mortgage at 7.5%. This along with housing construction, which plummeted in 2022 and 2023, as interest rates as well as material costs rose, has left the United States approximately half of its normal housing inventory. This has left those trying to buy homes to participate in bidding wars, all of which have kept housing prices surprisingly high.

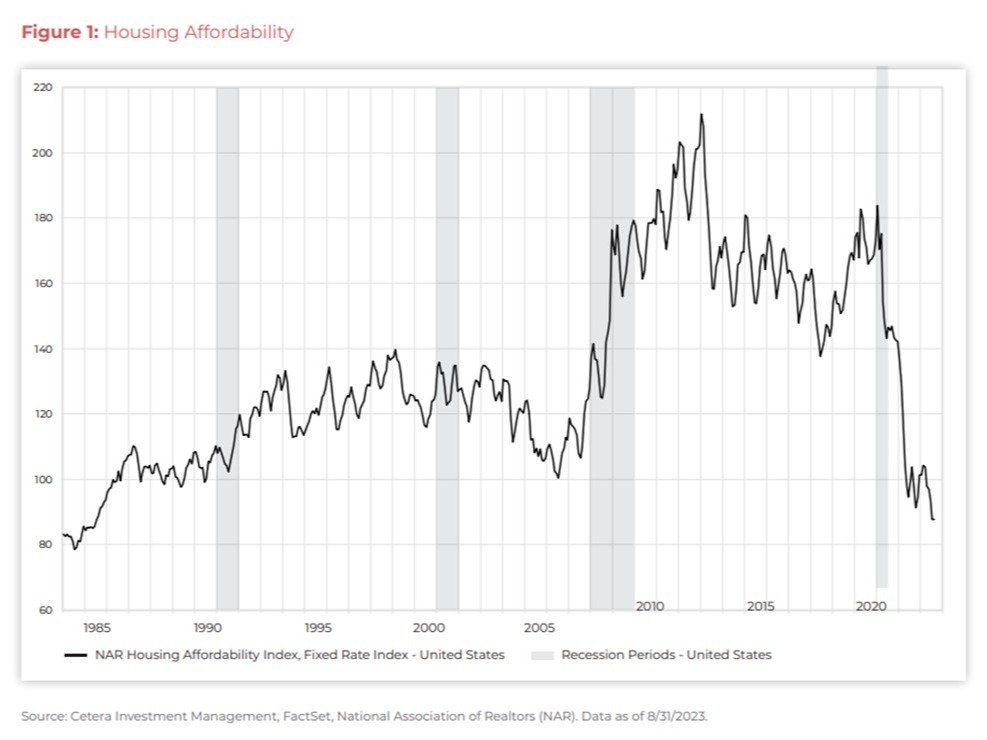

The combination of significantly higher prices and rising mortgage rates has driven housing affordability to its lowest level since the mid-80s, when mortgage rates were double digits, as you can see in our chart below.

Information from the National Association of Realtors shows that these factors have pushed the monthly mortgage payment for the same home up more than 80% over the last three years. This is devastating for young families who have to come up with a down payment on a much higher-priced home, and then also be able to afford monthly mortgage payments that are much higher than they would have been just a few years ago. This is putting the American dream of homeownership out of the realm of many.

There are two pieces of good news in the housing market today. However, they both apply only to existing homeowners. The first is since adjustable-rate mortgages make up less than 10% of all mortgages today, these higher interest rates are not impacting existing homeowners. As you can see from our second chart, the effective mortgage rate for current homeowners is only 3.6% compared to 7.5% for new mortgage applications today.

The second piece of good news is that the risk of mortgage foreclosure and default seems to have dropped dramatically, especially when compared with the subprime mortgage crisis in 2007–2008. 39% of homes today are paid off and have no mortgage debt. Homeowner equity is now 71% of the $52 trillion housing market, the highest percentage since 1960. Additionally, homeowners, who locked into lower mortgage rates over the last 10 years have built significant equity in their homes, as they have gone up in value, leading to a much lower risk of default.

As we look at the economy and the markets today, we must wonder if Fed Chairman Jay Powell feels a lot like Professor Wayne Szalinski. The big difference is that Fed policies blew up the mortgage rates and payments, not the kid. Unlike Disney, we hope that the Fed does not produce a sequel. As always, If you have questions about your own housing situation, or if you have children or relatives struggling with these issues, please let them know we are here to help. It is our goal and our mission as we continue “Moving Life Forward.”

© 2023 Jesse Hurst

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot directly invest in indices.