One of the most common questions I hear as a financial planner is, “How much should I have saved by now?” And often, people asking are in their 50s. The reason they are asking in their fifth decade, is that is when retirement starts to feel real. College expenses may be winding down, your career is likely established, you may be an empty-nester and for many people, this is the first decade where they truly begin looking ahead at what retirement could actually look like.

Source: iStock.com/Jacob Wackerhausen

You’ve probably seen articles saying you should have five or six times your salary saved by age 50, and closer to eight to ten times your salary by age 60. Those benchmarks can be helpful as general guidelines, but I don’t think they tell the full story, and may ignore pension income. I’ve worked with people who had less saved than the “recommended” amount and were still in great shape for retirement, while others had large account balances but weren’t nearly as prepared as they thought. The reason is simple: retirement is personal, therefore you need a personal, customized financial plan.

What matters most is not necessarily how much you have saved compared to someone else, but whether your savings align with the lifestyle you want to live. Someone who plans to spend $70,000 per year in retirement needs a very different plan than someone who wants to spend $200,000 per year traveling the world, buying a second home, or helping support charities, children and grandchildren.

Your timeline matters too. Retiring at 62 looks very different from retiring at 70. Even working a few extra years, or working part time, can dramatically improve a retirement plan because it gives your investments more time to grow while shortening the number of years your savings need to support you. Social Security, pensions, rental properties, or even part-time work in retirement can also play a major role in how much you truly need saved.

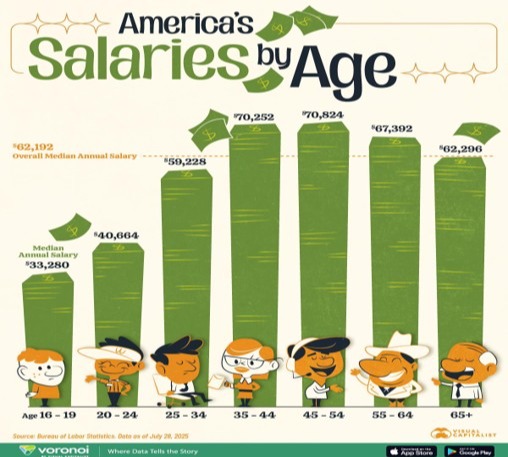

For many people in their 50s, this is also the decade where earnings peak, as shown in the chart above. That creates a huge opportunity for additional retirement savings. If you feel behind, you still have time to make meaningful progress. I often tell clients that your 50s are less about perfection and more about intentional decisions.

Increasing retirement contributions, taking advantage of catch-up contributions in retirement accounts, paying down debt, and avoiding major investment mistakes can make an enormous difference over the next ten to fifteen years.

And honestly, many people are doing better than they think. I see individuals become discouraged because they compare themselves to unrealistic numbers online, without considering the full picture. What’s more important is understanding your own plan. Do you know what you spend? Do you know what retirement may realistically cost? Have you accounted for healthcare, taxes, inflation, and income sources? Those questions matter far more than whether you hit an arbitrary savings benchmark.

I also think people underestimate the emotional side of retirement planning. I’ve met retirees with millions of dollars saved who still constantly worry about running out of money, and I’ve met others with more modest savings who feel completely confident because they understand their plan and live within their means. Financial peace rarely comes from chasing a number alone. It comes from having clarity.

Your 50s are really the time to get serious about that clarity. This is the decade to stop guessing, stop lifestyle inflation, and start planning intentionally. If you know where you stand today, you still have time to adjust course if needed. And if you’re already on track, this is when planning shifts from simply building wealth to protecting it and using it wisely.

At the end of the day, there is no magic number that guarantees a successful retirement. The right amount is the amount that supports the life you want to live. The key is making sure your financial decisions today are moving you closer to that goal. I can help you bridge the gap between now and retirement to achieve your goals.

Irene Zurowski CFP® CRPS®

Financial Advisor

Securities and advisory services offered through Cetera Advisors LLC, member FINRA/SIPC, a broker/dealer and a registered investment adviser. Cetera is under separate ownership from any other named entity. 2006 4th Street, Cuyahoga Falls, OH 44221

All investing involves risk, including the possible loss of principal. There is no assurance that any investment strategy will be successful.

Distributions from traditional IRAs and employer sponsored retirement plans are taxed as ordinary income and, if taken prior to reaching age 59½, may be subject to an additional 10% IRS tax penalty.

Cetera Advisors LLC exclusively provides investment products and services through its representatives. Although Cetera does not provide tax or legal advice, or supervise tax, accounting or legal services, Cetera representatives may offer these services through their independent outside business. This information is not intended as tax or legal advice.

Featured Blog Image Source: iStock.com/Gearstd