"It's Good to Be King" is a song by rock singer-songwriter Tom Petty. It was released as the third single from his 1994 album Wildflowers. The song deals with the phenomenon of rock and roll stardom and has been described as elegant and folk-rock-ish. It includes the following lyrics, where Petty dreams about how awesome it would be for everybody if he really was king:

Source: IMDb

Yeah, the world would swing, oh, if I were king

Can I help it if I still dream time to time

If you need a reminder or would simply like to hear Tom sing about how great royalty would be, a YouTube video from the now 30-year-old song is included below.

Tom Petty - It's Good To Be King

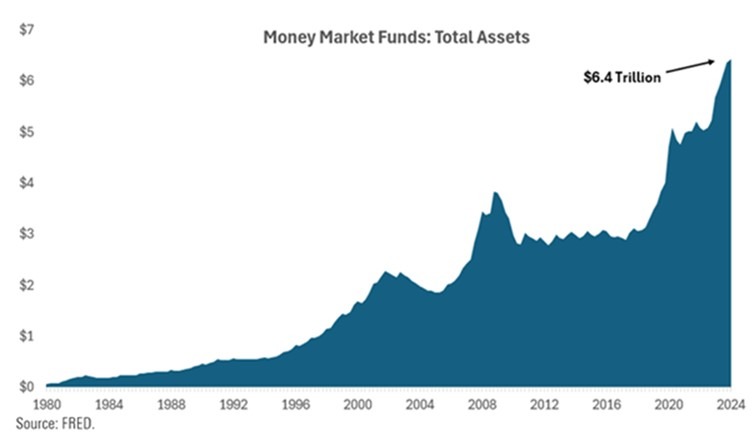

After more than a dozen years of lingering near the bottom of asset-class returns, cash, which would include investments such as money market funds, bank accounts, CDs, and treasury bills, must feel like king based on how popular they are and how much in the way of assets they have accumulated over the last couple of years. As you can see from our first chart below, the amount of money held in money market funds more than doubled from the early days of the pandemic to now.

In my more than 30 years of experience as a Certified Financial Planner, the money clients set aside in these types of investments typically spikes during times of fear. When people are afraid that the economy is heading into a recession or the stock market is going to have a downturn, they typically sell stocks and move the money into the safety of these cash-type assets. You can clearly see this in the chart above as the amount of these funds spiked after the economic and investment dislocation of events such as the dot.com bubble and 9/11, the ’07-’08 Great Financial Crisis, and the onset of the COVID-19 pandemic in early 2020.

In contrast, the most recent rise in assets was not driven by fear; it was driven by yields not seen in many years. This came on the heels of the Federal Reserve Bank raising interest rates at the fastest pace in nearly 40 years from March ‘22 to July ‘23 to combat persistent and rising inflation. Since the Fed first cut interest rates to 0% in December ‘08 in the wake of the subprime mortgage crisis, it had been rare to see yields above 2% on these types of lower-risk, lower-volatility investments. However, as the Fed drove short-term yields above 5%, savers and those seeking a safer place to get yields not seen in several decades moved their excess cash there in droves.

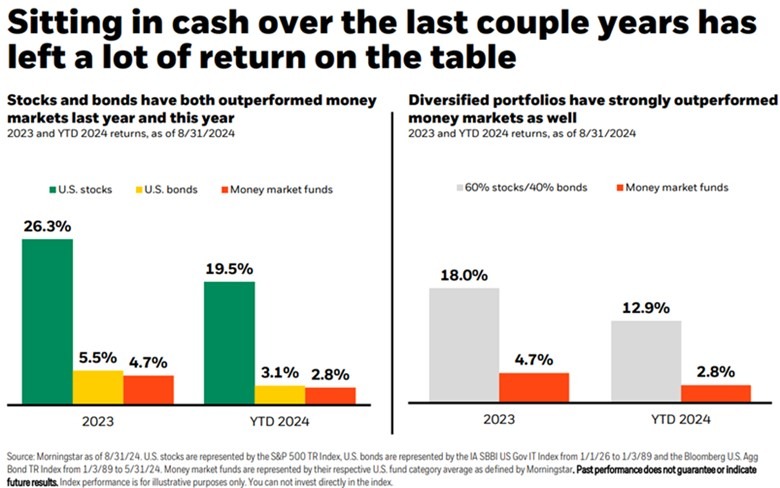

But was cash really king just because you could get higher yields than you were used to? Great question. Let's look at our second chart below to determine how dollars invested in money market funds performed compared to their stock and bond alternatives.

As you can see in the chart above, provided to us by our friends at Blackrock and Morningstar, money market fund performance significantly trailed the performance of U.S. stocks, as measured by the S&P 500 index, and that of a more typically diversified portfolio of 60% stocks and 40% bonds. This means that people who lived through the painful downturn in both the stock and bond markets in 2022 and then sold when markets were low and moved their funds to the perceived safety and yield that money market funds and cash were offering compounded their pain.

In September, the Fed cut interest rates for the first time since March 2020, during the COVID-19 pandemic. The Fed is projecting that it will cut rates two more times this year and four times next year. This begs the question, “What will happen to the yields on my money market funds if the Fed follows through with these interest rate cuts?” We know that money market fund yields will start to fall in concert with decreases in the Fed funds rate, which highly correlates to yields in the Treasury Bill market.

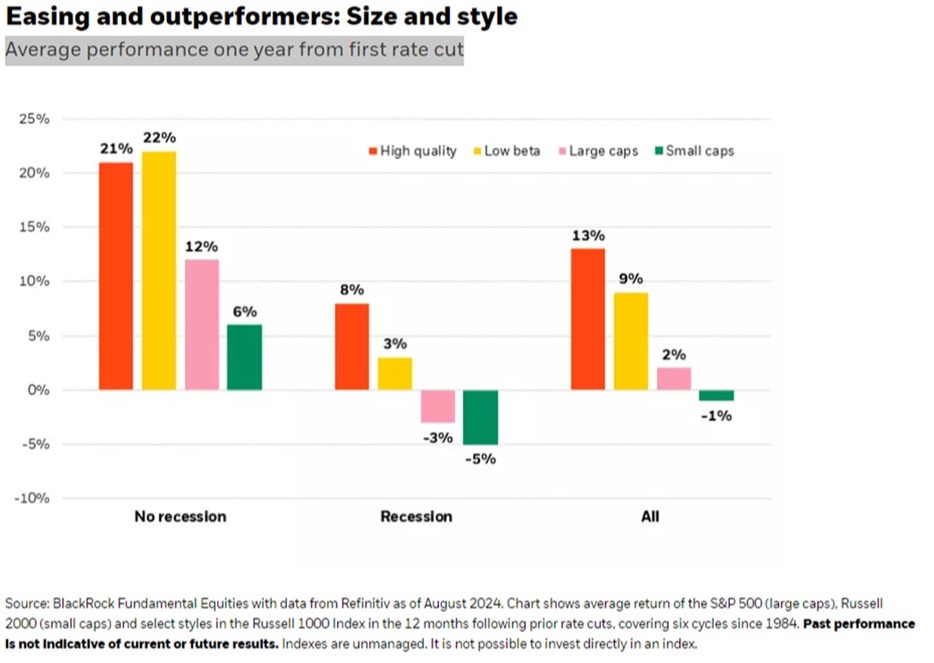

What about other asset classes? On a historical basis, we know that stocks tend to do well in the first 12 months after the Fed starts cutting interest rates if this does not coincide with a recession. The chart below shows the results for large-cap and small-cap stocks, as well as lower-beta and higher-quality stocks if the interest rate cut is or is not followed by a recession.

What about bonds? We know that bond prices generally go up when interest rates go down. This is what I call the “teeter-totter effect”, and I wrote about this extensively when the Fed started raising interest rates aggressively in 2022. You can check out my thoughts about that topic in the blog post, Will the Bond Market Give Us a Cherry Bomb??

https://www.impelwealth.com/blog/will-the-bond-market-give-us-a-cherry-bomb

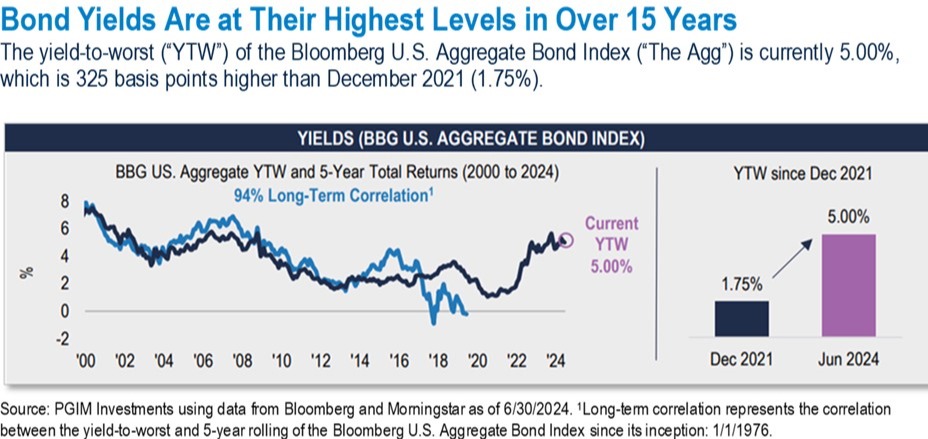

We also know that the aggregate bond market is paying interest rates higher than we have seen in more than 15 years. You can see this in our final chart below. This means we are getting reasonable yields and have the potential for appreciation if the Fed follows through and cuts interest rates, as they have said they will.

It's good to be king and have your own way

Get a feeling of peace at the end of the day

And when your bulldog barks and your canary sings

You're out there with winners, it's good to be king

While many clients and investors have been happy to get yields on their excess savings that they have not seen in many years, the charts and information above clearly show that cash is typically not king. This does not mean you shouldn't have some cash. As our retired clients know, the CFPs of Impel Wealth Management like our clients to keep two to three years' worth of liquidity in the money market, short-term, and limited-term bonds. This allows us to be patient and ride out the inevitable ups and downs of the market without having to sell assets low during times of volatility and dislocation.

We also know that having enough cash in the money market funds and liquid bank assets allows people to “Get a feeling of peace at the end of the day”, as our dearly departed friend Tom Petty would say. As my good friend Mark Bass, CFP extraordinaire in Lubbock, Texas, likes to share, “Clients live through market volatility better if they have enough sleep at night money!” I always learn when I'm in the presence of Mark, who has been in the business since 1974.

I thought this was a fun way to talk through current market conditions and historical asset class returns. As always, the CFPs of Impel Wealth Management are here for you if you have any questions as we continue “Moving Life Forward.”

© 2024 Jesse Hurst

Senior Wealth Manager

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/incomible