In the classic 1980 comedy movie Airplane!, which Rachel wishes I did not find so amusing, there isa pivotal scene when former military pilot Ted Striker has to summon all of his inner courage to focus on landing the commercial aircraft. He and Elaine, his ex-girlfriend, the flight attendant, are flying, as the pilot, copilot and navigator have all fallen ill due to food poisoning.

Source: YouTube

As he takes the controls of the airplane, he hears an inner voice telling him to concentrate:

Elaine - Dr. Rumack says the sick people are getting worse, and we're running out of time.

Ted - I've got to concentrate, concentrate, concentrate.

- I've got to concentrate, concentrate, concentrate.

- Hello? Echo!

- Pinch hitting for Pedro Borbon, Manny Mota. (BASEBALL BAT CRACKS AND CROWD CHEERS)

As the voices in his head overtake his conscious thought, he demonstrates how difficult it is to concentrate. For those of you who don't remember the scene, or for those of you who do and are simply looking for a humorous start to your day, a quick YouTube video to the classic scene is included below.

Airplane! - I've Got To Concentrate

However, the stock market is NOT having this issue. Over the last few years, the stock market, as represented by the S&P 500 index, has become more and more concentrated in just a few tech and AI stocks that have seen their earnings grow faster than the rest of the market. This has led to the 10 largest stocks in the benchmark to account for 37.7% of the index, which is the highest we have seen since 1990, as you can see in our first chart below, from FactSet and Bloomberg.

We all know that trends do not last forever. If they did, it would be easy for everybody to get rich. From my vantage point, not everybody is rich, so therefore, it must not be that easy. At some point, the high-flying earnings of these companies will moderate toward historical norms, while other parts of the market that have recently lagged will start growing again creating a new rotation and set of opportunities in the market. Recent evidence suggest that we may be nearing one of these inflection points.

Our friends from ClearBridge and Franklin Templeton recently pointed out:

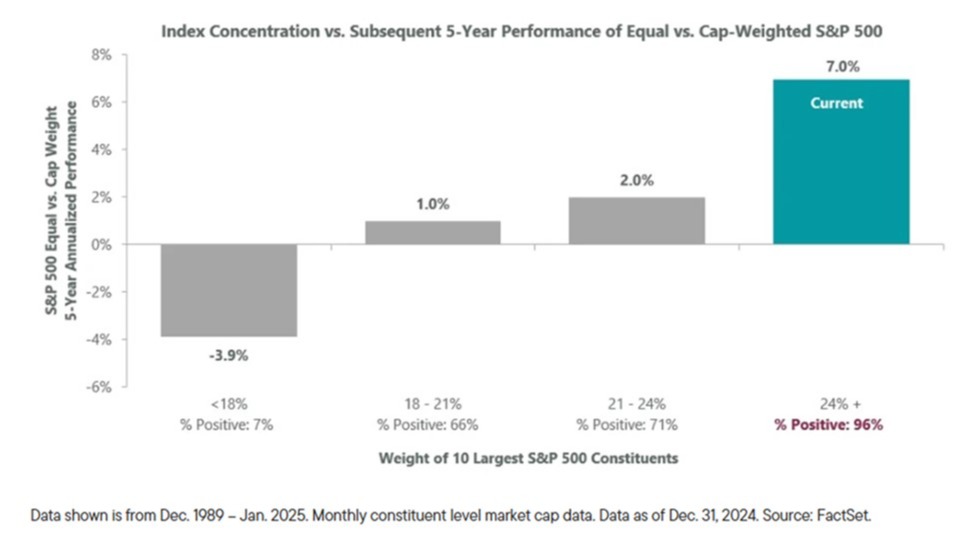

“If history is a guide, some of today’s perceived winners will in fact deliver on their promise and become key players in tomorrow’s landscape, while others will fall by the wayside. This presents an opportunity for active managers relative to passive benchmarks, which cannot sidestep this potential mean reversion. In fact, when the top 10 weights in the S&P 500 have accounted for over 24% of the benchmark, the equal-weight S&P 500 has outperformed its cap-weighted counterpart by an average of 7.0% (annualized) over the next five years since 1989, with positive relative returns occurring 96% of the time”, as you can see in our second chart below.

This would lead us to believe that now may be a good time to allocate some of your hard-earned resources to less loved and less expensive areas of the market. We accomplish this by staying disciplined in our diversification and rebalancing our portfolios on a regular basis. Doing so keeps us from having too many eggs in any one basket. We may not make a killing, but we will also likely not get killed in the process.

By the way, this is not just a US phenomenon. As you can see in our final chart below, which dates back to 1995, the United States now represents 56% of the global equity market valuation.

One thing you may note from the chart above is that earnings and market cap tracked very closely to each other until the last 10 years. Since then, share prices have grown much faster than the underlying earnings that support them. At some point, this will likely mean revert, and lead to a period when US large cap dominance is not so pronounced, giving other less loved areas of the market a chance to grow and shine. We never know when this will happen. This is why diversification remains an important cornerstone of successful portfolio management.

Ted Striker showed us how difficult it was to concentrate when he was trying to land a movie airplane. Over the last 10 years, the stock market has become more and more concentrated. This will likely end at some point and present new opportunities for those who don't chase the hot stock or the attractive improbability. The CFPs of Impel Wealth Management will continue to focus on asset allocation and diversification strategies that will help our clients reach their investment and retirement goals. We feel this is our mission and our purpose as we continue “Moving Life Forward.”

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices. A diversified portfolio does not assure a profit or protect against loss in a declining market.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Featured Blog Image Source: iStock.com/seamartini