"Money (That's What I Want)" is a rhythm and blues song written by Berry Gordy and Janie Bradford. Barrett Strong first recorded the song in 1959. In the US, the single became Motown's first hit in June 1960, making it to #2 on the Hot R&B Sides chart and #23 on the Billboard Hot 100.The song was listed as number 288 on Rolling Stone's "The 500 Greatest Songs of All Time”. The song gained recognition through cover versions by many artists, including The Beatles in 1963.

Source YouTube

The song developed out of a spontaneous recording session at the Hitsville Studio A in Detroit. Berry Gordy and Barrett Strong began by improvising on piano and vocals and were joined by Benny Benjamin on drums and Brian Holland on tambourine. It is a response song to the standard The Best Things in Life Are Free. Authors Jim Cogan and William Clark only identify the guitarist and bass guitarist as "two white kids walking home from high school [who] heard the music out on the street and wandered into Hitsville [and] asked if they could play along." They add, "Strong claimed he never saw the two boys who played bass and guitar again."

The Beatles recorded "Money" in seven takes on July 18, 1963, with John Lennon providing the lead vocals. Producer George Martin later added a series of piano overdubs. The song was released in November 1963 as the final track on their second UK album, With the Beatles, and subsequently released in the US in April 1964 when it was included on The Beatles' Second Album. According to George Harrison, the group discovered Strong's version in Brian Epstein's NEMS record store (though not a hit in the UK, it had been issued on London Records in 1960).

For those of you who are unfamiliar with these recordings that are more than 60 years old, I have included a YouTube link to each version of the song below.

Barrett Strong - Money (That's What I Want) (Lyric Video)

Money (That's What I Want) (Remastered 2009)

The song's lyrics express a desire for money, contrasting it with other things, such as love, highlighting the necessity and power of financial resources. The lyrics include the phrase "Your love gives me such a thrill, but your love don't pay my bills" to emphasize this point. Many Americans express a strong desire for wealth or financial gain. It can represent an aspiration for financial success, a focus on material possessions, or even a sense of desperation or ambition related to monetary matters.

For those of you who are interested in being a millionaire and would like to know what habits allowed people to become one, our friends at Hartford Funds put together a fact sheet entitled 10 Things You Should Know About Millionaires. I have included a link to the two-page document in this blog post. Below, I will share a few facts from their fact sheet along with some additional thoughts and observations that I have from my more than 35 years as a financial advisor.

First of all, there are a lot more millionaires out there than people would probably guess. In our country alone, there are approximately 24.5 million millionaires, which is approximately 9.4% of the US population. Globally, there are 62.5 million people whose net worth, defined as assets minus liabilities, exceeds $1 million. Approximately 41% of them live in the United States, as you can see in the chart below.

Source: UBS Wealth Report

Source: UBS Wealth Report

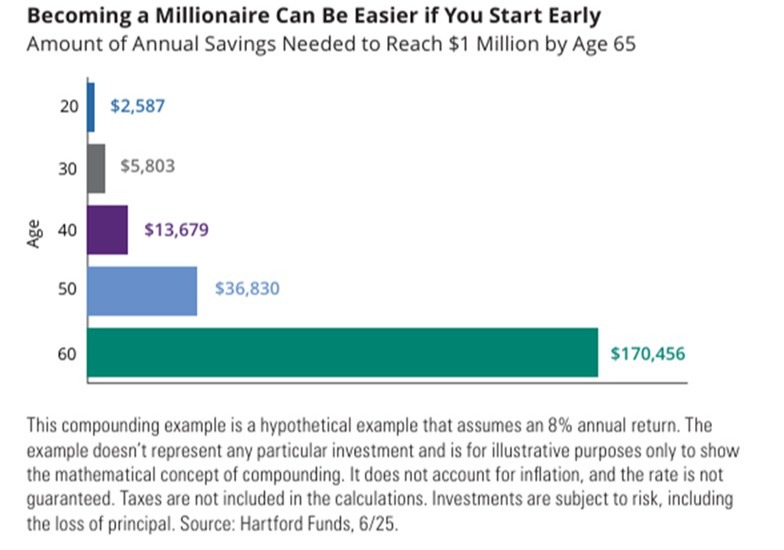

The second thing I would like to point out from the attached fact sheet is that most people become millionaires slowly. Just like many of our friends and clients who are reading this blog post, the compounding effect of good habits over long periods of time results in the accumulation of wealth. Fidelity points out that the average employee who has accumulated $1 million or more in their 401K plan has been contributing to it for 26 years. They have dollar cost averaged into their retirement account every paycheck, whether the economy was good or bad, and whether the stock market was moving up or down. The sooner they started and adhered to these principles, the easier it was to build significant wealth in their retirement accounts, as you can see in our second chart below.

The age demographics of millionaires also bear out this thesis. Approximately 66% of them are between 60 and 79 years old, and approximately 23% are between the ages of 50 and 59. Many of you have heard me reference the book The Millionaire Next Door multiple times in our conversations over the years. It appears that the majority of millionaires adhere to principles from the book. Most don't spend ridiculous amounts of money on things they can't afford or have to finance on credit cards. They don't spend money on expensive cars, flashy clothes, and vacations. Instead, they spend less than what they make, they save and invest regularly, they pay down debt quickly, and they don't make crazy investment decisions based on tips they get at the golf course or online.

Finally, it is essential to remember the compounded effect of inflation and life expectancy on your retirement resources. The fact sheet points out that 40 years ago, in the 1980s, having a net worth of over $1M put you in the upper levels of the financial echelon. Thanks to 40 years of inflation, you would now need more than $3M today to equal what $1M would be in 1985. This is why the CFPs of Impel Wealth Management always show your projected net worth in both absolute dollars and inflation-adjusted dollars in our retirement plan projections.

Even though the song's lyrics tell us Money (That’s What I Want), we have found that what most people want is to accumulate the resources necessary to do the things that they find important in life. I thought these facts and observations on millionaires would be an interesting way to remind you, or reconfirm to you, what it takes to join the $1M net worth club. I also think this would be an excellent way to share with your younger family members who have the time to build the habits necessary to create their own financial success. Remember, we are here for them as well as we continue “Moving Life Forward”.

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/Olga Arsentyeva