A recent report from the National Association of Realtors showed that the median age for first-time homebuyers in the United States reached an all-time high of 40 years old. This is up 10 years from age 30, just over a decade ago, as you can see in our first chart below.

The same report indicates that delaying homeownership from age 30 to 40 can result in a loss of approximately $150,000 in equity on an average starter home. Most young families build wealth by accumulating home equity as property values rise and mortgage balances decrease, and consistently contributing to their 401(k) plans.

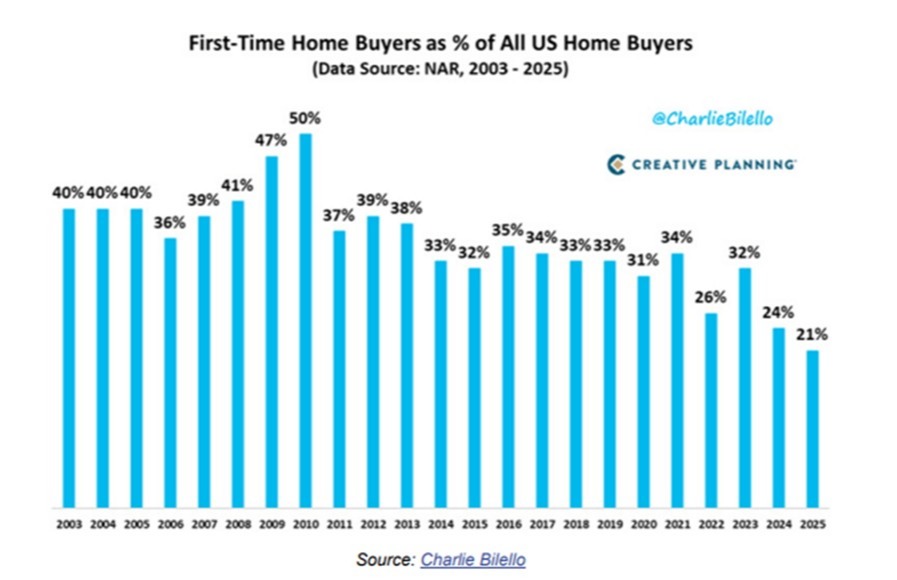

Similarly, the percentage of first-time homebuyers among all US home purchases has declined. As shown in our second chart, about one-third of new home purchases were made by first-time buyers a decade ago. Today, that figure has dropped to 21%.

I discussed this in my recent blog post, The Housing Perfect Storm.

https://www.impelwealth.com/blog/the-housing-perfect-storm,

There are many reasons for these alarming statistics. These include home prices rising dramatically over the last 15 years, and especially since the COVID-19 pandemic. Mortgage rates have more than doubled over the last five years, and homeowners' insurance and property tax rates have risen significantly. And most importantly, the amount of money needed for a down payment and to qualify for a mortgage has risen faster than wages, pricing many young families out of the market.

The government has been absolutely no help in making homes more affordable for would-be purchasers. In many parts of the country, regulatory costs and delays associated with building a home have driven up prices and reduced the supply of new homes. There are a few notable exceptions, such as Austin, Texas, where a reduced regulatory environment has allowed home building to flourish. This has driven inventory up and prices down, and should be a model for other cities and states to consider.

Monthly mortgage payments are significantly higher today due to the factors mentioned above. In response, President Trump recently proposed creating 50-year mortgages, which could lower monthly payments and improve affordability for prospective buyers. As a real estate developer, the President is accustomed to debt and often introduces unconventional ideas.

As expected, the proposal generated immediate and varied opinions. Many articles quickly appeared, debating whether 50-year mortgages are beneficial or problematic.

Today, I will present some of these perspectives using a Point/Counterpoint format. I previously used this approach to discuss the federal government and the Federal Reserve Banks' response to rising inflation in a three-part series from June 2021, available on the blog section of the Impel Wealth website.

For context, in the early 1970s, the CBS news program 60 Minutes featured a recurring segment called Point Counterpoint, where two reporters debated opposing sides of an issue. Saturday Night Live also parodied this format in its Weekend Update segments. Examples of both can be found on YouTube.

Source: YouTube

POINT

Regarding 50-year mortgages, some reporters, including one in a November 12th Bloomberg News article, argue that these loans are not necessarily a bad idea. They note that lower monthly payments could make homeownership more accessible for young families.

The reporter reasons that very few people stay in their house for 30 years and keep their original mortgage. Typically, people move or refinance in under 10 years. This reporter viewed the 50-year mortgage as a gateway to getting into the housing market.

COUNTERPOINT

However, most people in the financial planning world had a different take on the 50-year mortgage. Even though homes would be more affordable with lower payments, it doesn’t take a math major to figure out that the interest cost of these longer mortgages would be a significant burden on consumers looking to build equity from their home ownership.

Financial commentator Jared Dillian detailed the additional interest costs in his November 13th newsletter.

For example, with a 30-year fixed mortgage at 6.5% on a $400,000 loan, total interest paid over the life of the loan would be $510,178. This exceeds the house's original cost.

However, by moving to a 50-year mortgage, the total interest payments increase to $952,921. Yes, your monthly mortgage payment drops from $2,528 to $2,254. This does save $274 on your monthly mortgage payment. However, you end up paying an additional $412,000 in interest over time.

This leads Jared to ask the following question:

In what universe does this sound like a good idea?

I have always shared with you that math matters and that we should pay attention to what the numbers tell us. In this case, I strongly agree with Jared. Paying more than $400,000 in additional interest to save less than $300 per month does not make good financial sense. The only way I would consider it is if you thought it would help you get into the homebuyer market, with the idea that you would refinance to a 15- or 20-year mortgage in short order once you had built some equity in the house, to reduce your overall payments and interest costs.

Point/Counterpoint

It was notable how quickly opinions diverged on this issue.

If you receive questions from friends or family about 50-year mortgages as a means to improve affordability, I hope this background and context are helpful.

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

- What Should I Do With My Inherited IRA?

- Decluttering More Than Closets: Why Organizing Your Financial Life Matters

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/olm26250