In the book The Runway Decade, my good friends and business partners from Baton Rouge, financial advisors Pete Bush and Bill Bush, provide an insider's look at simplifying the complex process of retirement planning. The basic premise is that once you enter your 50s, you have approximately 10 years of runway left before you take off into your retirement journey. It is an excellent book and a unique way to approach planning for a successful retirement. It is filled with many great examples and anecdotes. I strongly suggest you pick up a copy at the link below and consider these lessons as you continue your own journey.

Source: Amazon.com

Well, it seems that Social Security is also in the midst of its own “Runway Decade”. In mid-May, the Trustees of the Social Security trust funds issued their annual report on its current and projected financial status. This program is foundational to most retirees' income. As in previous years, they found that Social Security continues to face significant funding issues. This could potentially affect the benefits you receive in the future.

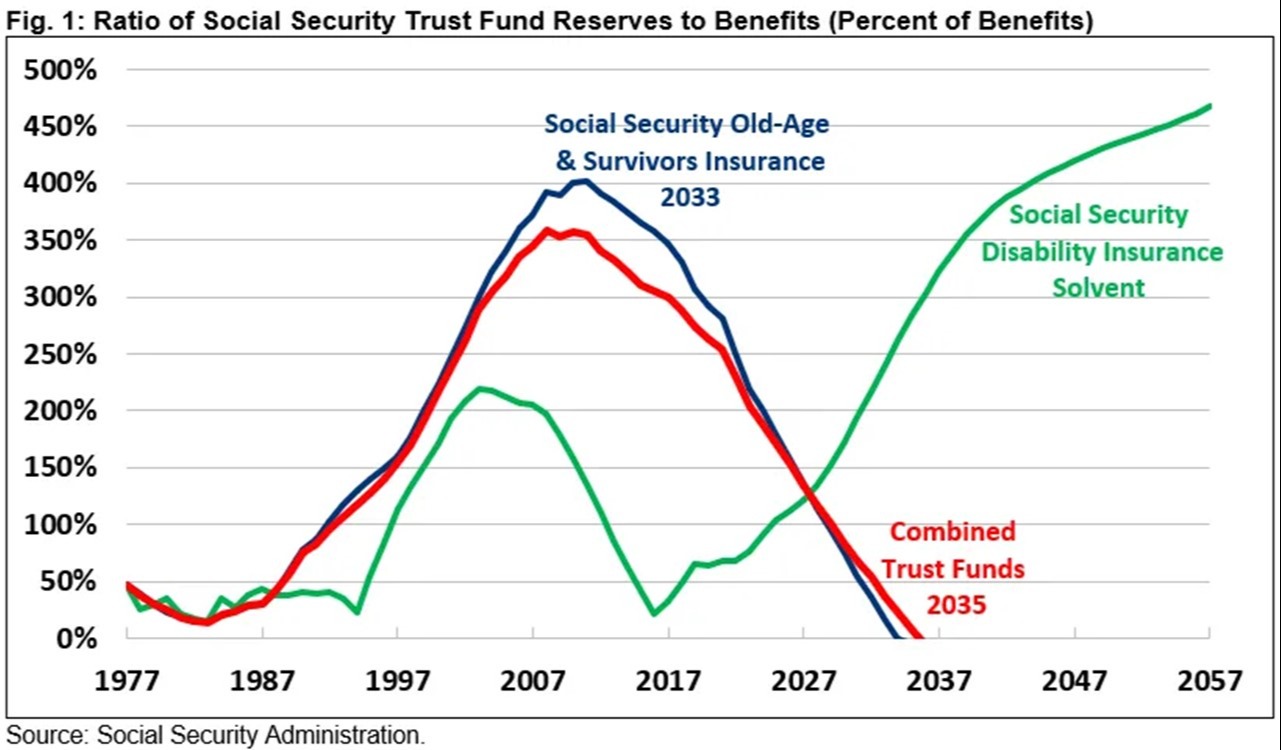

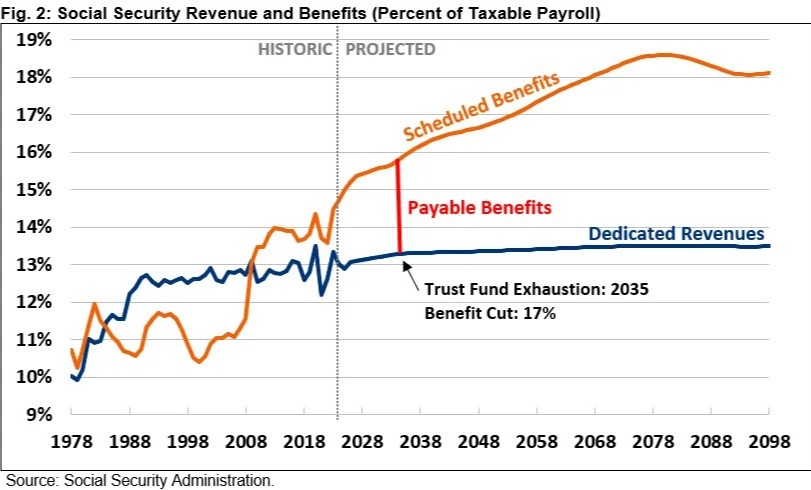

While this is very frustrating, it is not a new challenge. I have been writing about this for at least the last ten years. The current report shows that the trust fund will be able to pay 100% of its total scheduled benefits until just 2033. This is unchanged from last year's report. At that time, the fund's surplus reserves will be depleted, and the continuing FICA and self-employment taxes being paid into the system by current workers will only be sufficient to pay 79% of the scheduled benefits.

Please remember the last time adjustments were made to Social Security was in 1983. At that time, a Commission appointed by President Ronald Reagan and headed by future Federal Reserve Bank Chairman Alan Greenspan recommended changes to help Social Security meet the future challenge of funding future benefits to the very large baby boomer generation. These included raising the FICA tax paid by both employees and employers and gradually raising the age at which you could collect full Social Security benefits from 65 to 67 years old.

This allowed Social Security to bring in more tax revenue each year than the benefits it paid out. This resulted in a surplus, which continued to grow until the Great Financial Crisis in 2008 when AIG and Lehman Brothers failed. At that time, many people who expected to continue working until age 65 or longer lost their jobs and began collecting Social Security benefits early, as you can see in the chart below. The combination of not paying FICA taxes during their working years and receiving their Social Security benefits early started to deplete the accumulated funds.

According to the 2024 trustees report, Social Security will run cash deficits of $3 trillion over the next 10 years. Over the next 75 years, the actuarial shortfall will rise to $24 trillion in present value terms. Again, this is not new news. The Social Security trustees, as well as economists and CFPs, have been shouting from the rooftops for many years that this future crisis needs to be addressed sooner rather than later.

Policymakers only have a few years left to take the necessary steps to make Social Security solvent for future generations. The longer they wait, the more difficult and costly it will be to fix. Acting sooner rather than later will allow lawmakers to consider a broader range of options and provide more time to phase in changes. This will allow future retirees to have more time to prepare for retirement.

As we consider “Social Security's Runway Decade”, we have every right to be frustrated with the people we elected to Capitol Hill. Instead of constant investigations and bickering, it would be great to see bipartisan solutions to issues that affect everyday people. There are a number of potential levers that could be pulled in some combination, to fix Social Security. I will address these in Part 2 of this blog post. My goal is to keep you informed as we continue “Moving Life Forward.”

© 2024 Jesse Hurst

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Feature Blog Image Source: iStock.com/Piotr Mitelski