The band Boston released its self-titled debut album in August 1976, which was an instant smash hit, becoming the best-selling debut record in U.S. history at the time. The "Boston sound" blended melodic, classically inspired structures with guitar-driven hard rock. The resulting sound was unlike anything else on the radio at the time. The album was dominated by hits including "Foreplay/Long Time,” “Rock & Roll Band," and "Peace of Mind." Decades later, almost every track remains a staple of classic rock radio.

Source: Wikipedia

"More Than a Feeling" was released as the lead single and the opening track from the album in September 1976, with "Smokin'" as the B-side. Tom Scholz wrote the entire song. The single entered the US Billboard Hot 100 on September 18 and peaked at #5. The track is now a classic on rock radio, and in 2008, it was named the 39th-best hard rock song of all time by VH1. It was included in the Rock and Roll Hall of Fame list of the "500 Songs That Shaped Rock and Roll" and was ranked number 212 on Rolling Stone's "500 Greatest Songs of All Time" list in 2021.

For those who would like a reminder of this song or simply want to take a musical stroll down memory lane, a YouTube link to the official HD video, featuring lyrics, is included below.

Boston - More Than a Feeling (Official HD Video)

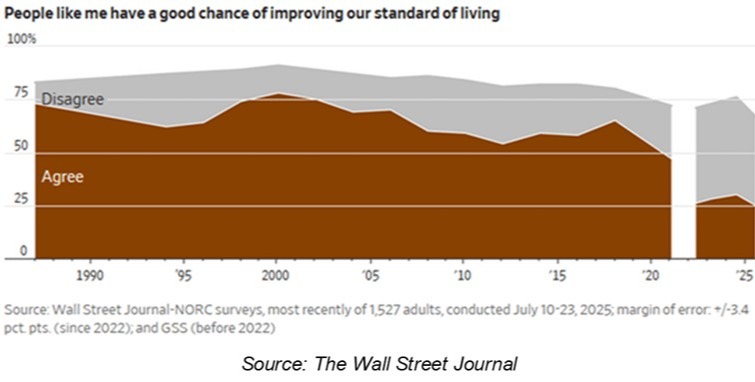

For generations, Americans had “More Than a Feeling” that hard work could lead to a better life. Today, though, that feeling seems less real. A recent Wall Street Journal-NORC poll reveals a significant shift in public sentiment: only 25% of Americans believe they have a good chance of improving their standard of living. Nearly 70% say the American Dream either no longer holds true or never did, as you can see in our first chart below.

You can see in the chart a significant drop following the COVID period, but a general downward trend is also evident even earlier. As recently as 2000, more than 75% agreed that they had a good chance of getting ahead; now, only 25% do, a decrease from last year’s survey. This isn’t just a blip. It’s a psychological and economic rupture that began before COVID but accelerated dramatically in its aftermath. Despite the most significant fiscal and monetary stimulus in history, consumer sentiment broke from historical patterns.

Something has gone deeply wrong in this century, and it’s getting worse. The discontent is widespread, cutting across all kinds of lines.

From WSJ:

“By large majorities, both women and men held a pessimistic view in the combined questions. Similarly, both younger and older adults, those with and without a college degree, and respondents with household incomes of more than $100,000, as well as those with less, reported similar results.”

“The poll found a somewhat brighter view of the current economy. Some 44% rated the economy as excellent or good, up from 38% a year ago, though still a smaller share than the 56% who now view the economy as not good or poor.”

“And yet many people in the survey, as well as in interviews, said they felt a sense of economic fragility, even if their finances were adequate or secure today. In a generational cascade, majorities said the prior generation had an easier time buying a home, starting a business, or being a full-time parent rather than in the workforce. At the same time, majorities also said they lacked confidence that the next generation could buy a home or save adequately for retirement.”

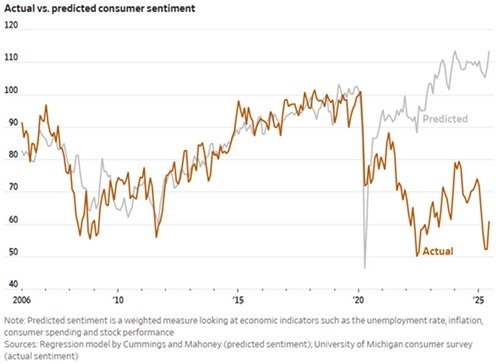

A model that once reliably predicted how people “should” feel based on unemployment, inflation, spending, and markets now diverges sharply from reality. People are far more pessimistic than the data suggests they should be. The chart below comes from the WSJ. The darker line represents the Michigan Consumer Sentiment Survey. The lighter one is a simple model that uses the unemployment rate, inflation, consumer spending, and stock market performance to predict how consumers “should” feel, given the historical correlations between these factors. As you can see, the model performed quite well from 2006 to 2020. Sentiment was predictable for each month’s prevailing conditions. But then COVID broke it.

Source: The Wall Street Journal

What is causing this gap? In a word, it's confidence, or more precisely, the lack thereof. It is not just about inflation, interest rates, rising home prices, and student loan debt. There is a more profound loss of trust in the system. Younger people see their parents and grandparents, many of whom own homes, had steady jobs, and retired comfortably, and they do not see a clear way to achieve the same. Owning a home feels out of reach. Starting a business seems riskier than it did before. Even saving for retirement feels pointless. As a result, many individuals do not think they have the necessary cash flow to contribute to a Roth IRA or their employer's 401 (k) plan.

Data from the survey shows that this sense of disappointment affects everyone—men and women, people with or without college degrees, and those with high or low incomes. Even people who believe the economy is doing well right now feel that their own situation is fragile. They might feel safe today, but they do not think that will last.

While this is not a fun or uplifting topic to discuss, there is a potential solution to the financial and economic malaise that many people are feeling. I firmly believe that financial education and financial planning can offer people the pathway to a brighter and more confident future. Financial literacy is at poor and unacceptable levels among most Americans, especially those under age 30. Having a better understanding of basic financial concepts, such as managing debt, compound interest, and saving for the future, could help people feel that they have more control over their financial future.

Additionally, the financial planning process can help people chart a path forward toward their preferred financial future, regardless of where they are starting today. This is why the CFPs of Impel Wealth Management have created programs such as Simplifynance and our Second Opinion offerings.

Our Simplifynance program was specifically designed to meet the financial planning needs of people under 40. By combining the best of what technology and a financial advisor have to offer, you’ll gain personal guidance on topics like education planning, debt management, and retirement savings – with tools that make it easy to track your progress.

Links to both services are included below. We encourage you to share these links with any friends or family members who you know are struggling with the issues above and could use a roadmap and a dose of financial confidence. Remember, we are here to help.

https://www.impelwealth.com/simplifynance

https://www.impelwealth.com/second-opinion

It is important to have an understanding of what this might mean for the economy and financial markets in the future. Economics is really about how people behave, and that has changed significantly. Consumer behavior is primarily driven by sentiment and confidence. If people lack the financial resources to spend or believe their job is at risk, metrics such as retail sales will start to decline. It is essential to remember that consumer spending accounts for approximately 70% of all economic activity that comprises our GDP.

Unlike Boston, we think you need “More Than a Feeling.” You need action, education, and a plan that can help lead you to a brighter financial future. While post-COVID sentiment and confidence in our economy have shifted significantly over the last five years, we believe that financial education and financial planning can be the antidote to this dire outlook. As a friend or client of Impel Wealth Management, I wanted to remind you of this vital information as we continue “Moving Life Forward.”

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/Andreus