Carl Perkins knew a thing or two about rhythm. His rockabilly classic “Right String Baby, But the Wrong Yo-Yo” had a bounce to it—fast, catchy, and just a little bit off. The metaphor was simple: everything looks like it should work… but it doesn’t. You’ve got the right string, but the wrong yo-yo.

Source: YouTube

If you are not familiar with this rockabilly classic from one of the original members of the Million Dollar Quartet, along with Elvis Presley, Johnny Cash, and Jerry Lee Lewis, I strongly encourage you to click the link below and turn the music up loud. I trust you’ll feel better in 2½ minutes.

Carl Perkins - Right String Baby, But The Wrong Yo Yo 1956 (STEREO)

The Beatles loved it. They covered it, jammed on it, and like so much early rock, it borrowed from something older. Simple structure. Timeless message. And right now, the Federal Reserve might feel like it’s living inside that song.

The Fed is unique among global central banks. It doesn’t just have one job… it has two: price stability and maximum employment. Most of its peers focus primarily on inflation. One string. One yo-yo. The Fed is trying to keep two yo-yos spinning at once—and lately, one isn’t responding the way it used to. For the last 15 years, the spotlight has been squarely on inflation—zero rates, quantitative easing, and then the fastest tightening cycle in decades. Everyone has an opinion on whether the Fed got that side right.

But today, it’s worth shifting the focus to the other half of the Fed’s mandate, because the employment side is starting to look like the wrong yo-yo entirely.

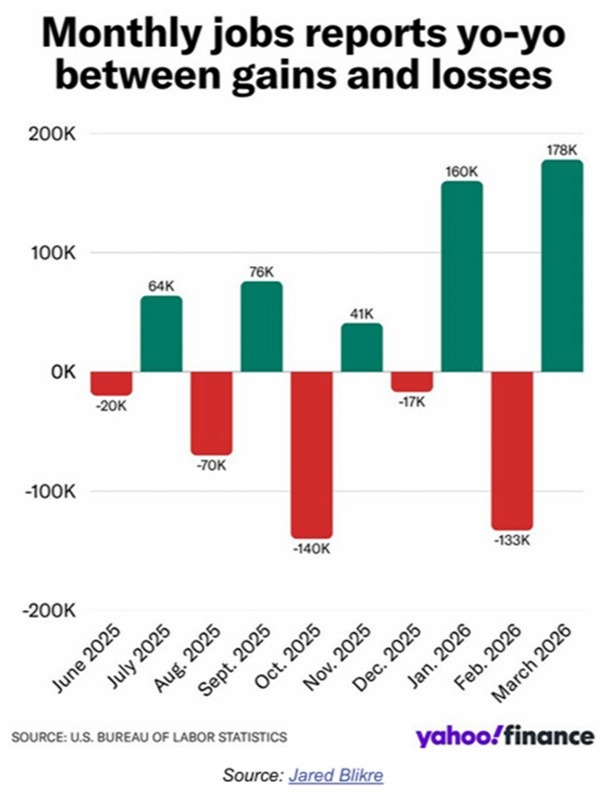

On the surface, the labor market still looks fine. Job growth has held up better than expected, unemployment remains relatively low, and there’s no obvious break. But just beneath that surface, the data is behaving in ways that don’t fit the old playbook. We’ve seen an unusual pattern of job gains and losses alternating month to month, as shown in our first chart below.

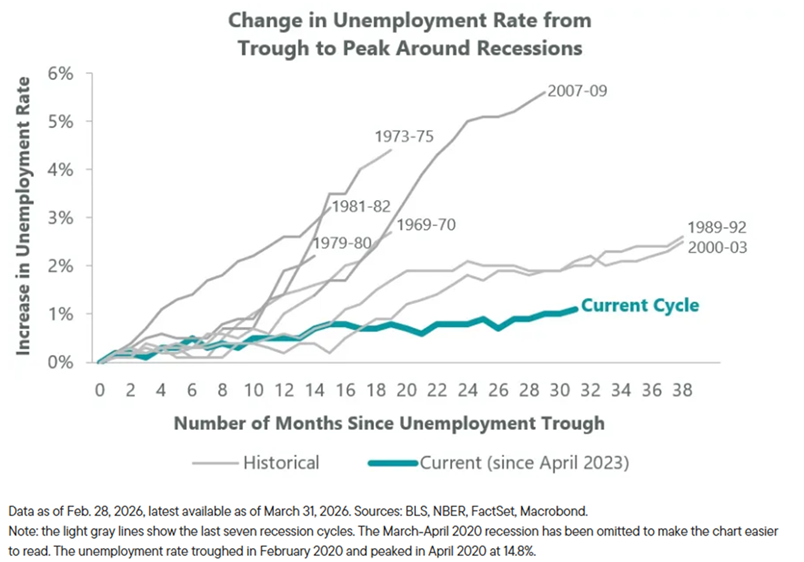

This pattern has occurred only a handful of times since 1939. That could be noise—but it’s happening at a time when the labor market is already acting strangely. Even more unusual, the unemployment rate has risen roughly 100 basis points from its 2023 low without a recession following. This has been the longest and slowest rise in unemployment that I have witnessed in my 38 years as a financial advisor, as shown in our second chart below.

Historically, that kind of move has been a warning shot, and it typically hasn’t taken this long to resolve. This time, the signal hasn’t led to the outcome everyone expected. Then again, economists have predicted 11 of the last 3 recessions… and the media may be even worse.

The reason may be simple, but uncomfortable: the constraint today isn’t demand for workers—it’s the supply of workers. For decades, the Fed’s models have assumed that if growth slows, unemployment rises, and if financial conditions tighten, hiring weakens enough to create slack. That framework worked in a world where labor supply was relatively stable. Today, it isn’t. We are dealing with structural forces that monetary policy can’t meaningfully influence, even if the Fed still acts as though it can.

The labor market isn’t weakening in the traditional sense—it’s tightening structurally. That makes Fed policy less effective and economic signals harder to interpret.

Start with demographics. Roughly 10,000 baby boomers reach retirement age every day. This isn’t cyclical. It’s not sensitive to interest rates. It’s a demographic reality steadily shrinking the available workforce. The Fed cannot create more workers by cutting rates, nor can it delay aging by tightening policy. The labor pool is simply getting smaller.

Layer on top of that the second major force: immigration policy. Over the last several years, the U.S. has experienced meaningful swings in immigration flows. Regardless of the politics, the economic impact is clear… immigration directly affects the size of the labor force. When inflows slow, the pool of available workers tightens further.

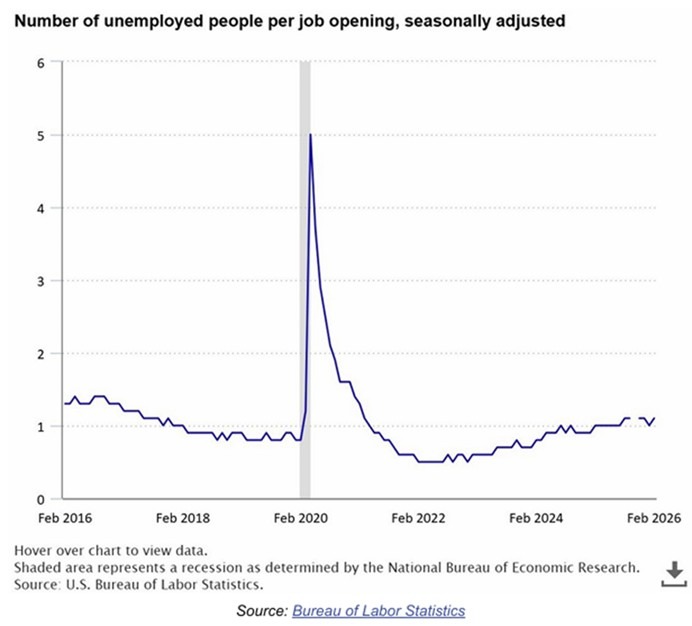

Put those two forces together, and you get a very different kind of labor market—one defined less by hiring booms and busts, and more by scarcity. Employers are slower to hire, but they are also slower to fire. When workers are harder to replace, companies become more cautious about letting them go. The result is a “low-hire, low-fire” environment where job creation cools, but unemployment doesn’t rise as much as traditional models would suggest. That helps explain why the labor market has remained more resilient than expected, even as growth moderates. It’s not that demand is surging… it’s that supply is constrained, as shown in our final chart of available workers per job opening.

Of course, no discussion of the labor market today would be complete without addressing artificial intelligence. The fear of an AI-driven job apocalypse is real and understandable. If machines displace workers faster than new jobs are created, the implications for income, demand, and profits could be significant.

But history offers a more balanced perspective. Every major technological shift has created disruption, but it has also created entirely new categories of work. In fact, only about 40% of today’s jobs existed 85 years ago. That’s a staggering reminder that job creation doesn’t just happen within existing industries… it often comes from places we can’t yet see. AI is already driving demand in areas like data infrastructure, energy, and advanced computing, and it is likely to expand into new domains over time. Creative destruction is rarely comfortable in the moment, but over the long term, it has been a powerful driver of growth.

Bring it all back to the Fed, and the Carl Perkins metaphor starts to feel a little too accurate. The Fed is still pulling on the string of unemployment—adjusting rates and financial conditions, expecting the yo-yo to respond the way it has in prior cycles. But the mechanism has changed. Demographics don’t respond to monetary policy. Immigration is set in Washington, not at the Federal Open Market Committee. Technological disruption follows its own timeline. The Fed may have the right string… its traditional policy tools, but it may be working with a very different yo-yo than the one it was designed to control.

For investors, this has important implications. It means we should be cautious about relying too heavily on historical comparisons when thinking about the labor market and the broader economy. It suggests that the Fed’s ability to “fine-tune” employment outcomes may be more limited than in the past, particularly when structural forces are doing most of the driving. And it reinforces the idea that periods of transition—especially those shaped by demographics and technology—tend to produce both confusion and opportunity.

The takeaway is not that the Fed is powerless. It still matters… a lot. But it does mean we may be asking it to solve for variables beyond its control. When that happens, policy outcomes become less predictable, and markets can misread both the data and the response function. That’s where discipline matters most.

Rather than reacting to every data point or trying to game the next Fed move, investors should stay focused on the bigger forces at work—aging demographics, evolving labor supply, and the long arc of technological change. These are the trends that will shape growth, earnings, and opportunity over the next decade, not just the next meeting.

Carl Perkins didn’t overthink it. Sometimes, the problem isn’t how hard you’re pulling… it’s what you’re pulling on. The Fed may still have the right string, but the yo-yo has changed. For investors, the message is simple: don’t get distracted by the string. Stay focused on the forces that actually move the yo-yo… and position for where it’s going. That’s how we keep “Moving Life Forward.”

© 2026 Jesse Hurst

Senior Wealth Manager

Related Conent

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/Easy_Company