I guess that some improvement is better than none. A recent survey from the Employee Benefit Research Institute estimated that approximately 41% of American households will not have enough money to live comfortably during their retirement years. That seems like a dismal forecast. However, it is a slight improvement over the same study from 2014 when 43% of households headed by people in the 35-64 age range were unprepared.

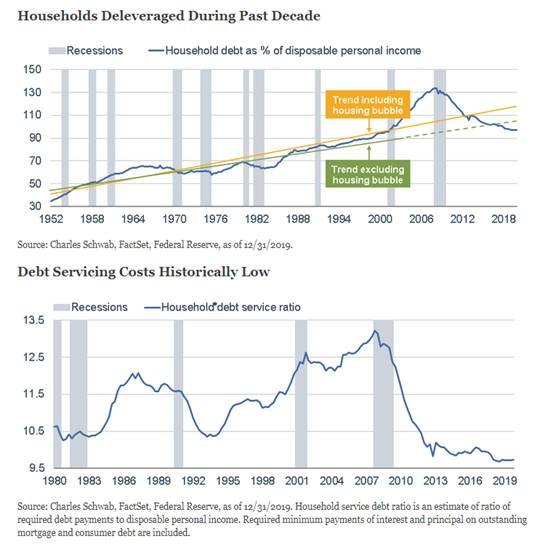

Some of the slight improvement seems to be due to the fact that people had seen their 401(k) plans and IRA's go up in value (FYI, the survey was completed before the COVID 19 viral outbreak). It should also be noted that individuals and consumers have not taken on significant new debt as the economy recovered from the Great Recession of '07-09. While student loan debt and car loan metrics are somewhat stretched, mortgage debt, home-equity credit lines and credit card debt have not soared as asset values have recovered over the last 10 years. It seems that individuals have had more restraint in their spending and debt levels than corporate America and certainly that US Government have.

|

There is another piece of somewhat encouraging news for those headed toward retirement. T Rowe Price conducts a study each year of Americans who participate in employer sponsored 401(k) plans. The results have typically confirmed that retiree's actual life experiences in retirement have exceeded their expectations from when they were working. The study asks people who have been retired for 10 or more years, "Given your savings, income and expenses, what has your experience been? "The answers have been very interesting. They show that 81% have enough money to pay for healthcare expenses, 72% live as well or better than when they were working and that 66% will be able to leave some inheritance to family members or a charity of their choice.

Not surprisingly, the survey found that there was a direct correlation between retiree satisfaction and the level of income and assets that retirees had built. At Impel Wealth Management, one of our goals is to help people accumulate the resources necessary to make the transition from work to retirement life successfully. Given our current health and economic landscape, converting these assets into a steady stream of income that will support your retirement lifestyle goals can be challenging. The distribution phase of retirement can easily last 25-30 years or more. Please reach out to us if you, a friend or loved one have questions about this process. We stand ready to help our friends and clients meet this challenge as we continue "Moving Life Forward".

© 2020 Jesse Hurst