Saving for a child’s future can feel overwhelming. College, housing, retirement—it’s a lot to think about when they’re still in diapers. That’s where Trump Accounts come in. This new type of investment account, created under the One Big Beautiful Bill Act, is designed to help families start investing for kids early—and let time and compound growth do the heavy lifting.

Launching in 2026, Trump Accounts aim to make long-term investing simpler and more accessible for families, while encouraging a habit of saving from day one.

So, What Exactly Is a Trump Account?

Think of a Trump Account as a long-term investment account for kids that blends features of a retirement account with the flexibility of a savings plan.

The money in the account is invested—usually in low-cost funds that track the U.S. stock market—and grows tax-deferred over time. Anyone can contribute: parents, grandparents, friends, employers, and even charities. The child doesn’t need a job or earned income to qualify.

The big idea? Start early, invest consistently, and let compound growth work its magic over decades.

Who Can Get One?

Trump Accounts are available for any child under age 18 who has a valid Social Security number. There’s no income requirement, no employment requirement, and no complicated eligibility rules.

The program officially begins in 2026, and contributions can start after July 4, 2026.

There’s also a nice bonus for some families: children born between 2025 and 2028 are eligible for a one-time $1,000 government contribution to jump-start their account. Free money that gets invested early? That’s a strong start.

How Much Can You Put In?

For the first couple of years (2026 and 2027), total contributions are capped at $5,000 per year per child, regardless of how many people are contributing. Starting in 2028, that limit will be adjusted for inflation.

Some contributions—like certain employer or government contributions—may not count toward that annual limit, depending on how final rules shake out.

The flexibility here is a big plus. Grandparents can chip in for birthdays. Employers may offer contributions as a benefit. Families can add money whenever it makes sense for them.

How Is the Money Invested?

Trump Accounts aren’t meant for risky stock picking or speculation. The rules require investments to be placed in low-cost mutual funds or ETFs that track broad U.S. stock market indexes, such as the S&P 500.

This keeps things simple, and focused on long-term growth—not short-term market swings.

The goal isn’t to time the market. It’s to stay invested and let growth build steadily over time.

What About Taxes?

Here’s where Trump Accounts really shine:

- Contributions are made with after-tax dollars (so no upfront tax deduction).

- The investments grow without being taxed year after year.

- When the child turns 18, the account is generally converted into an IRA, and standard IRA tax rules apply going forward.

In other words, you don’t get a tax break today—but you do get years (or decades) of tax-efficient growth.

Can the Money Be Used Before Retirement?

Trump Accounts are meant to encourage long-term saving, so withdrawals aren’t allowed until the child turns 18. After that, once the account becomes an IRA, withdrawals follow standard IRA rules.

That means taking money out early could trigger taxes and a 10% penalty, unless the withdrawal qualifies for an exception (such as education expenses or a first-time home purchase). Specific rules are still being finalized, so this is an area to watch.

Bottom line: this isn’t a piggy bank. It’s a long-term investment account designed to grow over time.

Why Starting Early Matters (A Lot)

The real power of Trump Accounts comes from time.

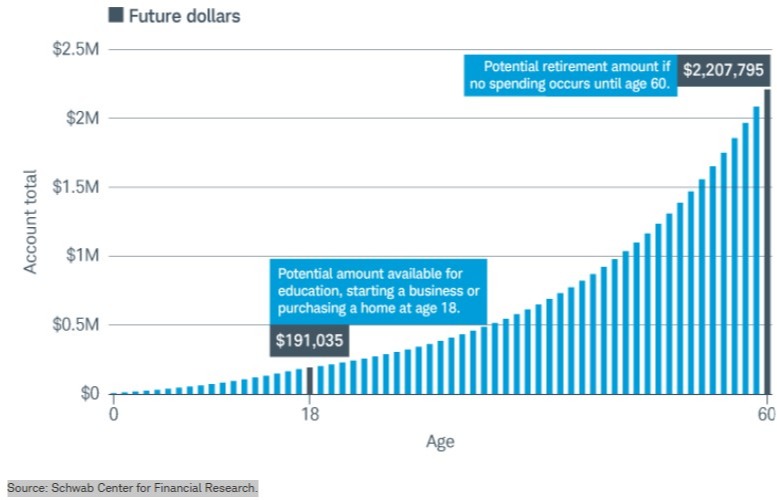

According to the example chart below from the Schwab Center for Financial Research, if a family contributes the maximum amount (adjusted for inflation) each year for 18 years—and earns an average annual return of about 6%—the account could grow to roughly $190,000 by the child’s 18th birthday, and much higher than that if the account stays invested into adulthood.

This is compound interest doing what it does best.

The hypothetical investment results shown are for illustrative purposes only and should not be deemed a representation of past or future results. Rates of return will vary over time, particularly for long term investments. Outcomes vary and are not guaranteed.

How Trump Accounts Fit With Other Savings Plans

Trump Accounts aren’t meant to replace everything else. Instead, they work best alongside other tools, such as:

- 529 plans for education-specific savings

- Roth IRAs for retirement-focused tax-free growth

- Traditional savings accounts for short-term needs

Families might use a Trump Account for broad, long-term investing while keeping other accounts for more specific goals.

The Bottom Line

Trump Accounts are a new and potentially powerful way to help kids build wealth early in life. With flexible contributions, tax-efficient growth, and even a government-funded head start for some families, they offer a compelling option for long-term planning.

That said, the program is still new, and some rules are still being finalized. If you, a family member, or friend have questions about how a Trump Account fits into your bigger financial picture, please feel free to reach out to our office. We thought this was important information to share with you as we continue Moving Life Forward together.

All investing involves risk, including the possible loss of principal. There is no assurance that any investment strategy will be successful. Past performance is not an indication or guarantee of future results. "Trump Accounts" are a new savings vehicle for children, established under recent legislation. For complete details regarding taxes on earnings and withdrawals, consult your tax advisor or attorney.

© 2026 Nathan Ollish

Senior Financial Advisor

Related Content

- Baby Steps and the Financial Planning Process

- Beyond College: Smart Ways Parents Can Save and Invest for Their Kids' Future

Securities and advisory services offered through Cetera Advisors LLC, member FINRA, SIPC, a broker/dealer and a registered investment adviser. Cetera is under separate ownership from any other named entity. For a comprehensive review of your personal situation, always consult with a tax or legal advisor. Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice.

Featured Blog Image Source: iStock.com/Colorfuel Studio