The Opposite is the 22nd and final episode of the fifth season of the television comedy Seinfeld. It aired on NBC on May 19, 1994. While having lunch, George tells Jerry that every decision he has ever made has been wrong and that his life is the exact opposite of what it should be. Jerry convinces him that "if every instinct you have is wrong, then the opposite would have to be right". George experiments with doing the complete opposite of what he would normally do. He orders the opposite of his normal lunch and introduces himself to a beautiful woman who happens to order the same lunch, saying, "My name is George. I'm unemployed, and I live with my parents." She is impressed and agrees to date him.

Source: Reddit

Thanks to his date, George gets an interview at the New York Yankees' headquarters, where he also does the opposite of his instincts and criticizes George Steinbrenner about his management practices, thus landing him the job of Assistant to the Traveling Secretary. He moves out of his parents' house. Enraptured with his success, he regards “The Opposite” as his personal philosophy.

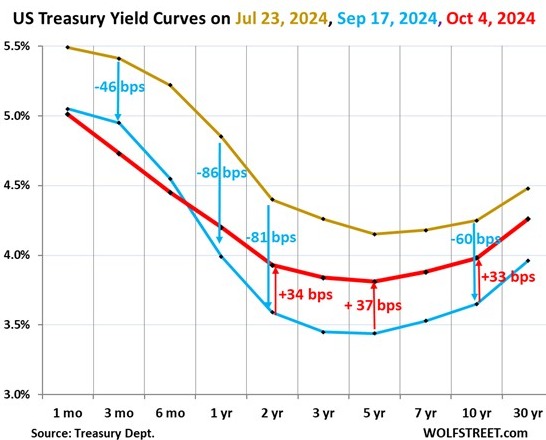

It seems like the bond market has adopted George Costanza's philosophy. You see, for the better part of 2024, economists and market strategists had been expecting the Federal Reserve to begin cutting interest rates. Early in the year, the Fed futures market anticipated as many as six 1/4 % rate cuts. The Fed finally cut interest rates at its September meeting by 50 bps. As typically happens, interest rates across the yield curve spectrum fell in advance of these well-telegraphed interest rate cuts. As you can see from our first graph below, interest rates on 2-year and 10-year treasuries fell by 81 bps and 60 bps from July 23rd to the Fed’s meeting on September 17th.

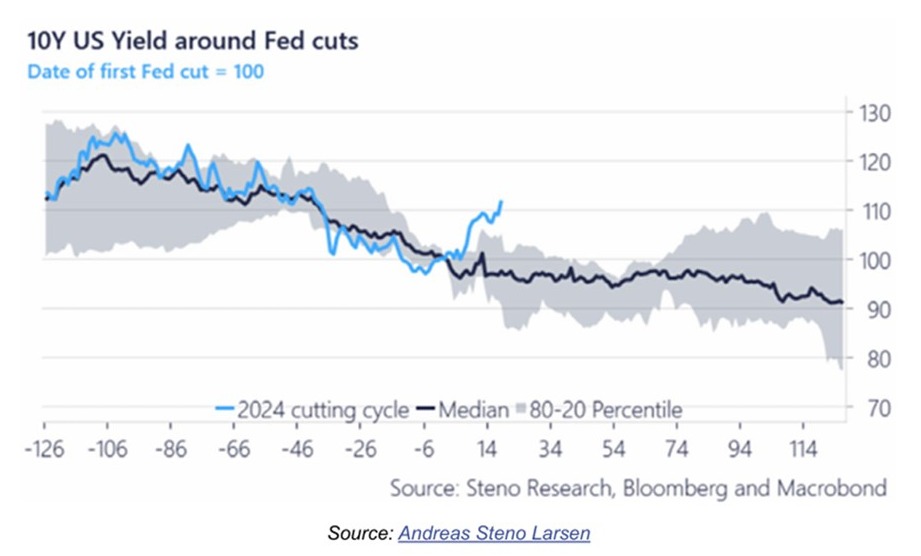

When examining historical data on interest rate cuts, we noticed that interest rates fall in anticipation of the Fed's first rate cut and typically continue to fall after the cut occurs. You will see that historical pattern in our second chart. However, it is essential to remember that the Federal Reserve Bank only controls short-term interest rates. The bond market determines longer-term interest rates, which are tied to things such as 30-year mortgage rates.

The 100 line in the chart above represents the date of the first Fed rate cut. The black line represents the typical trajectory of 10-year treasury yields, which have historically fallen after the first rate cut. The blue line represents what has happened this year. As you can see, the bond market seems to be taking its cue from our friend George Costanza and is doing “The Opposite” of what it has historically.

This has substantial implications for the economy and the impact of interest rates on consumer loans. The most important of these is what happens with mortgage rates. The day before the Fed cut interest rates in September, 30-year mortgages averaged just over 6.1% nationally. With the 10-year treasury doing “The Opposite” of what it typically has done, 30-year mortgages have climbed back towards 7%. This has disappointed people hoping to see mortgage rates fall so they could either refinance their homes or buy a new home with a lower interest rate.

Why has the bond market pushed interest rates higher while the Fed is finally trying to lower short-term interest rates? Great question. The financial news media is floating multiple theories. These include geopolitical risks, uncertainty around the election outcome, the economy and corporate earnings being stronger than is generally believed, and the rapidly rising level of government debt. The truth is nobody knows for sure.

Source: YouTube

Many people have been disappointed and confused to see interest rates for consumer and mortgage loans move up as the Fed embarked on its first rate cut campaign since the spring of 2020 during the COVID-19 economic shutdowns. The bond market has attempted to adopt George Costanza's philosophy, moving interest rates ”The Opposite” of what most people expected. I wanted to use some humor and provide context for you, our trusted friends and clients. I thought this was an important narrative to understand as we continue moving life forward.

© 2024 Jesse Hurst

Senior Wealth Manager

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/Simone_Capozzi