“You ain’t so big. You just tall, that’s all.”

Source: Spotify

Jimmy Reed’s Big Boss Man was never really about size. It was about power—who holds it, who answers to it, and how heavy it feels once you’re the one in charge. Elvis would later turn the song into a swaggering, cinematic moment in the largely forgettable movie Clambake, leaning into the sunglasses-and-attitude version of authority. But even then, the message stayed intact: being the boss doesn’t mean the job is easy. It just means everyone’s watching.

In 1990, the song was inducted into the Blues Foundation Hall of Fame. In its induction statement, blues historian Jim O'Neal noted that the song's appeal went beyond blues musicians, noting that “If there ever was a blues theme for the proletariat, it was Jimmy Reed’s 1961 smash, 'Big Boss Man.”

Source: YouTube

For your listening pleasure and to provide context for the rest of today's discussion, I have included YouTube links to both the Jimmy Reed version, complete with lyrics, and the Elvis Presley version of the song below.

Jimmy Reed - Big Boss Man (with lyrics) (1960) [HIGH QUALITY COVER VERSION]

ELVIS PRESLEY - Big Boss Man (New Edit Mix Version 2) 4K

As of January 30, 2026, Kevin Warsh is preparing to become the next Big Boss Man of American monetary policy.

Source: Wikipedia

President Trump’s nomination of Warsh to serve as Chair of the Federal Reserve didn’t land quietly. Markets immediately treated it as more than a personnel change. It was interpreted as a signal—perhaps the strongest yet—that a long-overdue shift in philosophy at the Fed may finally be underway.

Gold and silver reacted first…and forcefully. Gold dropped nearly 5% in a single session, while silver plunged more than 20% at its lows. These weren’t panic moves. They looked more like a market reassessing long-held assumptions about inflation, dollar credibility, and the durability of ultra-loose monetary policy.

Treasury yields rose, particularly on the long end, suggesting that investors are beginning to price in a smaller Fed balance sheet and less permanent intervention. Equities wobbled but remained composed. Historically, new Fed chairs often preside over early volatility, and this episode fits the pattern. The important takeaway wasn’t fear…it was recalibration.

For now, markets appear willing to give Kevin Warsh the benefit of the doubt.

That confidence is rooted in familiarity. Warsh served as a Federal Reserve Governor from 2006 to 2011, including during the Global Financial Crisis. He was present for the emergency decisions that defined an era. And in the years that followed, he became one of the most prominent critics of how those policies evolved…particularly quantitative easing, abundant reserves, and what he viewed as the Fed’s expanding footprint in markets.

That evolution has defined the debate around his nomination. Supporters point to his willingness to reassess and adapt. Critics note that he once supported the very tools he later condemned. Both can be true. In fact, that tension may be exactly what qualifies him for the job.

History offers a useful—and sobering—parallel.

When Paul Volcker took over as Fed Chair in 1979, inflation was raging, public trust in the central bank had collapsed, and the U.S. economy felt ungovernable. Volcker’s response was brutal by design. He allowed interest rates to rise above 20%, knowingly pushing the economy into recession to break inflation’s grip. Farmers drove tractors to Washington in protest. Homebuilders mailed him two-by-fours to symbolize a housing market frozen solid. He received death threats. Presidents pressured him relentlessly.

Volcker didn’t blink. He believed the institution’s credibility mattered more than his popularity…and more than his job. Years later, even his harshest critics acknowledged that the pain he endured restored the Federal Reserve’s authority for a generation.

Kevin Warsh’s challenge is different, but the echoes are unmistakable. Volcker confronted runaway inflation head-on. Warsh confronts the long shadow of extraordinary policy… years of balance-sheet expansion, market dependence, and blurred lines between monetary discipline and economic management. Neither man walked into an easy job. Both stepped into moments when the institution itself was under question.

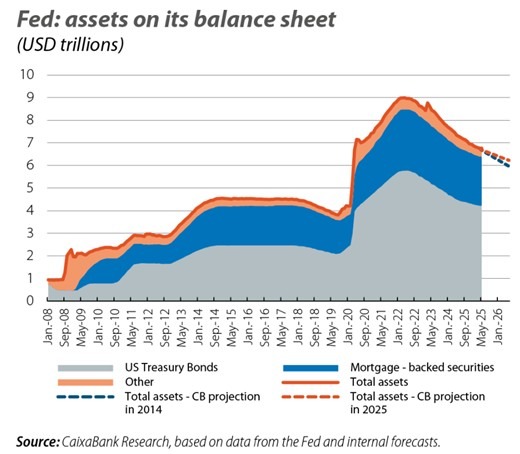

At the center of Warsh’s test is the Federal Reserve’s balance sheet.

Today, the Fed holds roughly $6.6 trillion in assets, primarily Treasuries and mortgage-backed securities accumulated through years of quantitative easing. These holdings suppressed long-term rates and flooded the system with liquidity. On the other side of the ledger sit bank reserves and currency in circulation…the grease that keeps modern finance moving.

Shrinking that balance sheet through quantitative tightening is straightforward in theory and treacherous in practice. Allow assets to mature without reinvestment, or sell them outright, and liquidity drains from the system. Long-term borrowing costs rise. Financial conditions tighten, and volatility typically increases.

Below, you can see how the Fed's balance sheet has increased dramatically in the 18 years since the Great Financial Crisis that led the Fed to start buying assets en masse.

The Federal Reserve Bank tried to to reduce the size of its balance sheet, unsuccessfully, in 2017 and 2018. They had more success over the last couple of years, but recently stopped this process and began buying treasuries to maintain liquidity in the markets. Not to mix musical metaphors, but this has led some commentators to say that quantitative easing and balance sheet expansion are like staying at the Hotel California, “You can check out anytime you like—but you can never leave.”

Warsh has argued that the Fed’s footprint has become too large and too permanent, distorting markets and encouraging excess risk-taking. It has also exacerbated wealth and income inequality, as those who own stocks and real estate have seen their asset values rise alongside these policies. Many policymakers agree with that diagnosis. The disagreement lies in execution. Shrink too slowly, and the distortions persist. Shrink too quickly, and something breaks.

That paradox defines the job. Despite the title, the Fed Chair is not an emperor. Warsh will hold one vote on a 12-member Federal Open Market Committee. He will need to rebuild trust with staff and fellow policymakers, some of whom he criticized sharply from the outside. Leadership here isn’t about issuing commands. It’s about persuasion, credibility, and institutional patience.

Then there’s the White House. President Trump has been clear about his desire for much lower interest rates. If Warsh delivers too eagerly, the Fed’s independence will be questioned. If he resists, political pressure is inevitable. Walking that line without damaging the institution may prove to be his most difficult challenge.

Layered on top is Warsh’s belief that AI-driven productivity gains could allow faster growth without inflation. If that thesis holds, it provides room to maneuver. If it doesn’t, the trade-offs become stark—and unavoidable.

For investors, this moment isn’t about predictions or positioning. It’s about awareness. Leadership changes at the Fed often reshape how markets think about liquidity, risk, and the safety net beneath asset prices. A smaller Fed footprint could mean less cushioning, more sensitivity to data, and a greater role for fundamentals. In other words, the Fed would allow capitalism and free-market forces to drive the economy, rather than the Fed always trying to take the wheel during periods of stress. That doesn’t have to be bad, but it does require adjustment.

Jimmy Reed’s Big Boss Man ends not with triumph, but with tension. Even Elvis, in full movie-star swagger, couldn’t escape the joke embedded in the song: the boss may look powerful, but he’s still bound by the job. Authority doesn’t free you. It binds you.

Kevin Warsh is stepping into a Federal Reserve that is more politicized, more scrutinized, and more consequential than at any point in modern history. This isn’t a role for bravado or slogans. It’s a role for steadiness, humility, and the willingness to disappoint just about everyone at some point along the way.

Being the Big Boss Man doesn’t mean you get your way. It means you own the outcome. Every decision. Every consequence. Every verse of the song. That’s the weight of the job.

Here’s wishing Kevin Warsh the clarity Paul Volcker found in crisis, the resilience to carry institutional responsibility, and, if we’re allowed one lighter hope, the wisdom to remember that even the Big Boss Man answers to the music eventually. I thought this was an important story and perspective to share as we continue Moving Life Forward.

© 2026 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/vDraw