After working as a financial planner for more than 35 years, I can tell you that Thomas J. Stanley and William D. Danko were right. There are significant differences between the habits of people who want to build wealth and people who want to live an affluent lifestyle. In 1996, they chronicled their research on this phenomenon in The Millionaire Next Door. Since its release, I have referenced this philosophy often when talking with clients. Many of my successful clients share the traits and habits that the authors use to describe people who are successful in building wealth.

Source: Medium.com

Their wisdom was top of mind in conversations I had with a couple of clients last week. Both of these clients are under the age of 60 but have set themselves up to make a successful transition from work life to retirement life when they would like. This does not necessarily mean that they will retire as young as possible. It simply means that they have accumulated enough resources so that if they continue working longer, it is because they want to, not because they have to. I have observed the following common traits that clients who have been successful in this endeavor share:

- No matter how much money they make, they spend less than they earn.

- They pay down debt quickly.

- They systematically save and invest in vehicles such as their 401k's and IRAs.

- They don't make unnecessary purchases on credit.

- They don't make investment decisions based on tips they got at the golf course or online.

The authors of the book also observed that most people did not inherit money. They built wealth through the good habits listed above. They paid attention to their budgets and expenses, meaning they were disciplined in their financial lives. Accumulating wealth does not happen by accident.

There is a big difference between income and wealth. Income is what you earn, while wealth is what you accumulate. Many people on both ends of the income spectrum never accumulate wealth, although for different reasons. Many higher-income people wonder why they aren’t rich—they feel they can barely keep up with expenses. They would likely not be able to survive more than a few months without a paycheck.

There is a social media phenomenon where people claim they are “bougie broke.” They post pictures of themselves wearing expensive clothes, eating out at expensive restaurants, or going on vacation to exotic locations while at the same time complaining about barely having enough money to get by or lacking the means to support what appears to be their extravagant lifestyle. For those of us old enough to remember rotary dial phones with something called telephone cords, “bougie broke” is akin to “keeping up with the Joneses.”

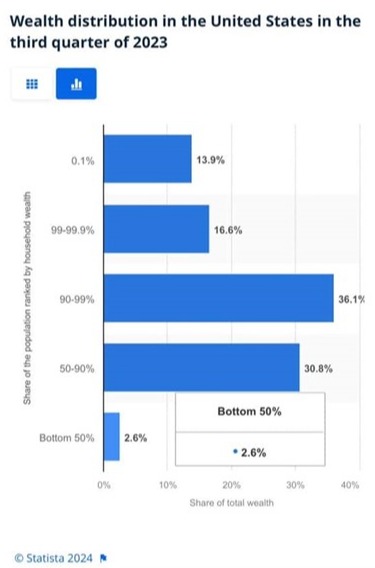

Spending habits like this are just one of the factors contributing to the growing wealth divide in the United States. The graph below, provided by Statista, shows that the top 1% of the US population holds approximately 30% of the country's wealth. The top 10% holds approximately 66% of all wealth, and the bottom 50% holds less than 3% of the wealth in the US.

It is interesting to note that during times of economic uncertainty or recession, the spending of those in the top 10% does not tend to fluctuate much, as they have resources to be able to afford what they want. However, factors such as job loss, economic downturns, or high inflation can have a significant impact on those in the bottom half of the graph above. These families are being forced into making real-life decisions about whether to fill up the gas tank so they can go to work or fill the prescription they need.

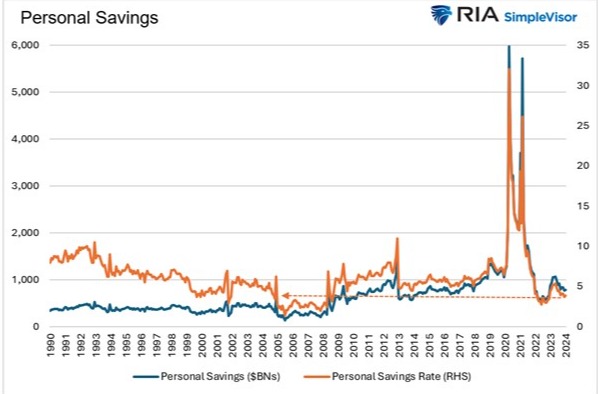

The Federal Reserve Bank’s Report on the Economic Well-Being of US Households from June 2023 stated that over 1/3 of US households do not have enough savings to cover an unexpected $400 expense. This is after significant stimulus checks and enhanced unemployment benefits were sent to most of these families during the COVID-19 coronavirus outbreak. This caused a temporary upturn in the savings of US households. However, as you can see from our next chart, these savings have come back down below their pre-COVID levels.

Source: RIA SimpleVisor

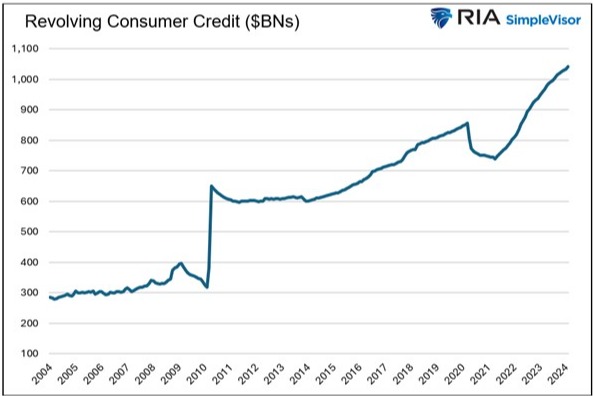

It is all too common for American consumers to continue buying even after they have depleted their cash reserves. This also means that many families would have to borrow or sell something to pay for an unexpected automobile or medical expense. Unfortunately, most people turn to credit cards rather than temporarily pulling back on their spending. As you will see in our final chart below, this has led to consumer credit card balances rising to the highest level on record after a temporary dip during the early days of COVID-19 when people could not go out and spend.

Source: RIA SimpleVisor

The wisdom of Thomas J. Stanley and William D. Danko is relatively straightforward and simple. However, we should not confuse simple with easy to implement. If it was easy, most people would be wealthy, and we know this is not the case. The CFPs of Impel Wealth Management are here to help you implement good habits and reach your goals. Living affluently may be fun until the bills come due.

We want to see you be wealthy and not just affluent. By the way, people who are successful in building wealth ultimately get to live a more affluent lifestyle. That is if you can get them to spend their money. As always, if you have friends or loved ones who are struggling with these issues, please send them our way, we would be more than happy to help them as we continue “Moving Life Forward.”

© 2024 Jesse Hurst

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/https://www.istockphoto.com/portfolio/berni0004?mediatype=photography