The members of the Horizon Advisor Network Investylitics Committee met on the afternoon of Monday, July 6th. It has certainly been an interesting first half of the year with multiple forces pushing and pulling on the markets and the economy. We were happy to have the opportunity to review portfolio performance over the first six months of the year and discuss the mid-year outlooks from the various economists and market strategists our committee follows.

June was a challenging month for the market as both the S&P 500 and the Nasdaq lost ground. In June, U.S. markets experienced a tech sector pullback that weighed on the major averages. The S&P 500 fell by 0.7%, while the tech-heavy Nasdaq Composite declined by 2.7%. Despite the monthly dip, both indexes logged massive gains in the first half of the year, with the S&P 500 up 9.6% and the Nasdaq climbing more than 12%.

We have continued to see a divergence between hard data and soft data in economic reports and surveys. Economic growth continues to come in stronger than expected. GDP is projected to be approximately 2.5% in the second quarter, both the manufacturing and service sectors are expanding, and the AI data center build-out continues at a record pace.

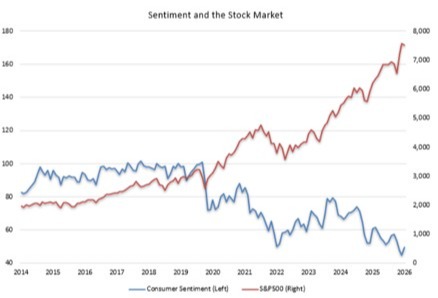

However, as you can see in our first chart below, consumer sentiment has continued to disconnect from both economic data and stock market performance. You will note that from 2014 until the COVID-19 lockdowns in 2020, consumer sentiment and the S&P 500 were much more closely correlated. This relationship broke down post-pandemic, and the gap has continued to widen despite a constructive economic backdrop.