"Take the Long Way Home" is the third US single from English rock band Supertramp's 1979 album Breakfast in America. It was the last song written for the album, being penned during the nine-month recording cycle. I was 14 years old and finishing my 8th grade year when the song was released in October of that year. The song played in heavy rotation on Top 40 radio stations during that fall and winter and reached number 10 on the U.S. charts.

Source: YouTube

According to its composer Roger Hodgson, “ I really believe we all want to find our home, find that place in us where we feel at home, and to me, home is in the heart and that is really, when we are in touch with our heart and we're living our life from our heart, then we do feel like we found our home. The song is a vehicle for reflection in which the sometimes-disappointing realities in our grown up lives can reflect in a not so positive way on the hopeful idealism of our youth.”

If you are unfamiliar with this song or would like a reminder, the YouTube link to the band’s official live version of the song is included below for your listening enjoyment.

Supertramp - Take The Long Way Home (Official 4K Video)

For families who have been trying to buy their first house, or to upgrade from their initial starter home to a larger house for their growing family, it has undoubtedly been “a long way home.” Since the beginning of the COVID-19 pandemic, housing prices across the United States have risen by 50% or more across most of the country. When interest rates began to rise sharply in 2023 in response to persistent and increasing inflation, the Federal Reserve Bank raised interest rates at the fastest pace in nearly 40 years, and mortgage rates went from below 3% to above 7% in short order.

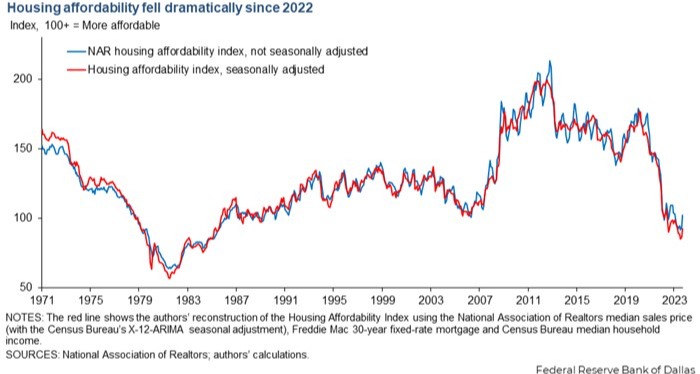

As you can see in the first chart below from the National Association of Realtors and the Federal Reserve Bank of Dallas, these two factors combined to put housing affordability at its lowest point since the mid-1980s. As homeowners who purchased their residences before interest rates started rising had locked in mortgage interest rates of 3 ½% or less, they were in no hurry to exchange their existing home for one at a much higher price point and a mortgage that was more than double their existing rate.

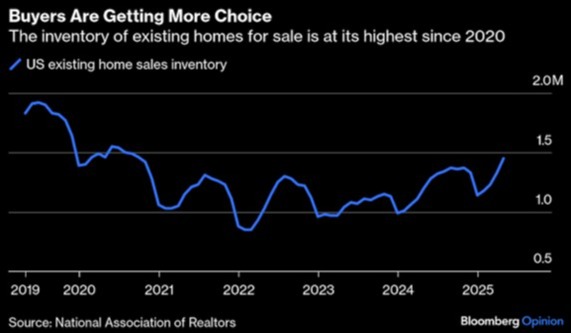

There was also a belief among existing homeowners that if they waited to sell their house, the price would continue to go higher. This belief has largely been borne out over the last five years. However, we are starting to see some anecdotal evidence of a shift in this dynamic. The enormous cost of homeownership, including property taxes and homeowners' insurance, both of which have increased significantly over the last few years, is starting to deter buyers. This is leading to a slow grind higher in the number of existing homes for sale. Over the previous two years, the number of existing homes on the market has grown by 40% and is moving towards levels not seen since 2020, as you can see in our second chart below. The trend of more homes on the market is not showing any signs of abating in the near future.

As is typical, all real estate is local, and the rise in residential inventory has not been evenly distributed across the country. Prices have continued to rise in the northeast and Midwest, sorry to those of you who live in Ohio. However, elevated inventory levels in states such as Florida and Texas have actually led to a decline in prices. According to the March S&P CoreLogic Case-Shiller U.S. National Home Price Index, only a handful of the 20 metropolitan areas tracked showed material home price increases. Home prices are falling in once-hot areas such as Phoenix, Denver, Atlanta, and Raleigh, and other regions are moving towards negative territory.

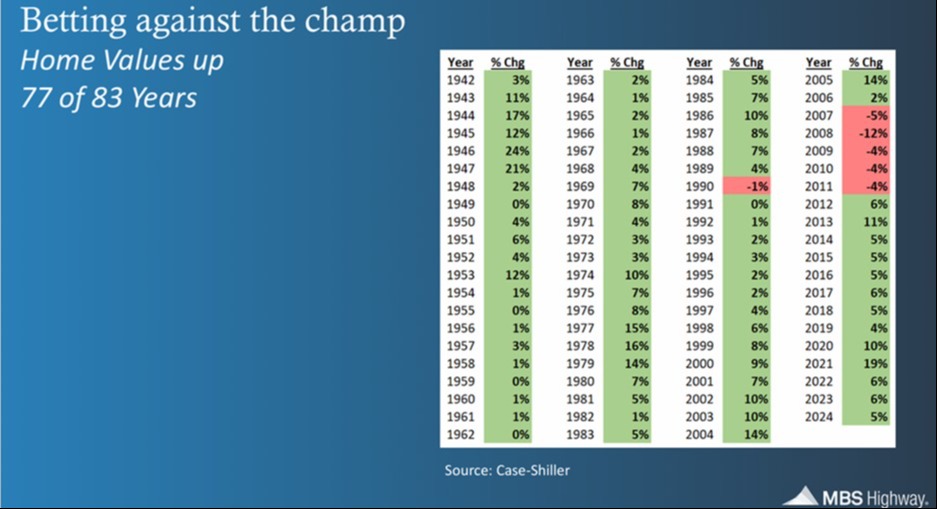

While we do not expect home prices to drop precipitously across the country, as we saw around the time of the Great Financial Crisis, more inventory is good news for those looking to make their first or next step in the housing market. As you can see in our final chart below, betting against housing prices rising over time has not been a wise wager. Home values have increased in 77 of the last 83 years. As a matter of fact, you can see that outside of the five years surrounding the subprime mortgage crisis, housing prices only dropped one other year, and that was a 1% drop in 1990.

Barry Habib is the founder of MBS Highway. Each year, Zillow asks 150 economists for their forecast on interest rates, inflation, mortgages, and house price appreciation. Barry has been awarded the Crystal Ball Award as the top real estate economist for four of the last seven years and has finished in the top five each year. That's why I listen when he talks. He recently said, “Let's take a broader view of the real estate market. There are 136 million households. 91 million are owned, 45 million are rented. Owners have $37 trillion in equity, with an average of $407,000. They got a lot. Renters, not so much. They've got zero. So please, the next time somebody says, well, it's cheaper to rent or pooh-poohs the housing market, please remember these statistics.”

We know that many young families have been forced to take the long way to get their first or next home. I wanted to provide some context around what might happen in the future as more inventory becomes available and how it may impact prices. It would still be helpful if interest rates cooperated and came down by a percent or so. However, with our current government debt situation, few see that in the immediate forecast.

Please feel free to share this information with your younger family members dealing with these issues. Please remember that the CFPs of Impel Wealth Management are here to help as we continue “Moving Life Forward.”

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/Ruhey