"Tighten Up" is a 1968 song by Houston, Texas based R&B vocal group Archie Bell & the Drells. The instrumental backing for the song was provided by the group T.S.U. Toronadoes, who had developed it in their own live shows before they brought it to Archie Bell & the Drells at the suggestion of Skipper Lee Frazier, a Houston disc jockey who worked with both groups. It reached No.1 on both the Billboard R&B and pop charts in the spring of 1968. It is ranked No. 265 on Rolling Stone magazine's list of the 500 Greatest Songs of All Time and is one of the earliest funk hits in music history.

Source: YouTube

Hi everybody

I'm Archie Bell of the Drells

Of Houston, Texas

We don't only sing but we dance

Just as good as we walk

I was first introduced to the song “Tighten Up” when I heard David Addison singing it on the TV show Moonlighting. For those of you who are unfamiliar with this song, or would like an early morning pick me up, I have included a YouTube link for your listening pleasure below.

Archie Bell & The Drells - Tighten up (1968)

In what may seem to be a strange coincidence, it appears that Federal Reserve Bank chairman Jay Powell, and his brethren at the Federal Reserve Bank, have been doing the “Tighten Up” for the last couple of years. However, at their October 2025 meeting, they told us they were going to stop. As you can imagine, doing the “Tighten Up” as the leader of the Federal Reserve Bank is significantly different than Archie Bell singing and dancing in the song above. Let me provide some background and context to help you understand what's going on and why it's important to you.

Most people are familiar with the fact that the Federal Reserve Bank tries to control the path of inflation, the rate of unemployment, and the general growth of the economy through raising or lowering the Fed Funds rate. This mechanism acts like either pressing the accelerator or the brake on the economy, dependent on what their current concerns are and what policy outcomes they are trying to achieve.

However, the Fed funds rate is just one of the tools the Federal Reserve uses to manage the economy, and hopefully, create its intended outcomes. Other tools used to manage monetary policy include quantitative easing (QE)/tightening (QT), forward guidance, and emergency measures. Today, we are going to focus on the Fed buying or selling longer term treasury bonds or mortgage-backed securities to try to raise or lower longer term interest rates in the market. This is known as quantitative easing or quantitative tightening.

The goal of quantitative easing (QE) is to stimulate the economy by lowering long-term interest rates and increasing the money supply, which encourages borrowing, investment, and spending. Conversely, the goal of quantitative tightening (QT) is to cool the economy by increasing long-term interest rates and reducing the money supply to combat inflation.

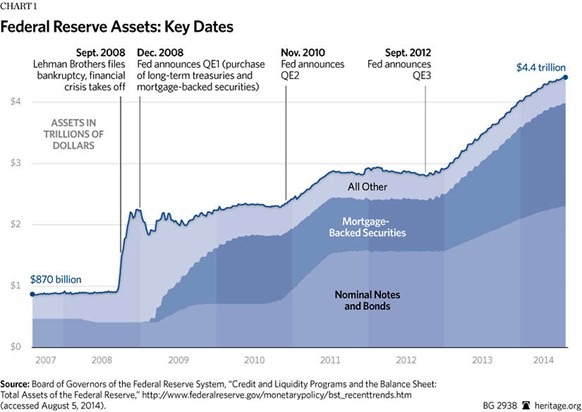

The Federal Reserve announced the first round of quantitative easing (QE1) in November 2008 in response to the Great Financial Crisis. The Fed conducted a total of three rounds of quantitative easing after the 2008 financial crisis, known as QE1, QE2, and QE3. The results of quantitative easing are debated among economists, with some studies pointing to its effectiveness in lowering interest rates and boosting asset prices, while others note its limited impact on broader economic growth and potentially negative side effects.

One thing we know for certain is that these multiple rounds of QE resulted in the Fed's balance sheet growing dramatically. Prior to the Great Financial Crisis, their balance sheet had typically been well below $1 billion and consisted primarily of short-term treasury securities. The Fed's three rounds of quantitative easing (QE) after the 2008 crisis involved large-scale purchases of long-term securities, causing its balance sheet to expand from less than $1 trillion to $4.5 trillion by 2014, as you can see in our first chart below.

Source: Heritage.org

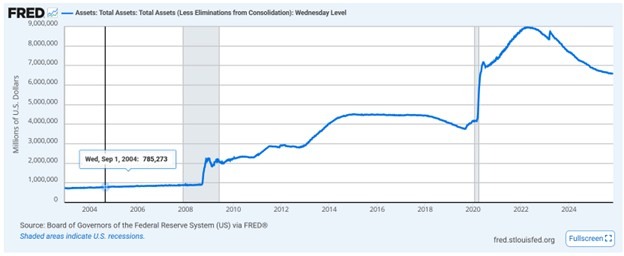

It was deja vu all over again in 2020 when the coronavirus pandemic shut down the US economy. Even though the Fed had not been able to successfully exit its previous rounds of quantitative easing and return its balance sheet to a more normal level, they decided to double down in the face of an unconventional financial and economic crisis. During the quantitative easing program launched in response to the COVID-19 pandemic, the Federal Reserve's balance sheet more than doubled, growing from under $4.0 trillion in March 2020 to a peak of $9.0 trillion in May 2022. This was achieved through the large-scale purchase of Treasury and mortgage-backed securities.

As you will see in our next chart, the Fed's balance sheet shot substantially higher in response to the initial COVID-induced economic shutdowns. It continued to grow over the next couple of years through multiple rounds of government stimulus programs, many of which were put in place even after there was strong evidence the economy was reopening and recovering from the pandemic shock.

Source: FRED

You will also see that the Fed's balance sheet which peaked at approximately $9 trillion in 2022, started retreating shortly thereafter. This is because the Fed reversed course and started doing the opposite, known as quantitative tightening (QT). You may notice in the chart above there was a slight reduction in their balance sheet in 2018. That was the first time the Fed tried to implement quantitative tightening, although it was not very well received by the financial markets at the time.

In Houston, we just started a new dance

Called the Tighten Up

This is the music

We tighten up with

The Federal Reserve has conducted quantitative tightening (QT) in two distinct episodes: the first from October 2017 to September 2019, and the second which began in June 2022. The Fed announced at their October meeting that this round of QT will be ending at the end of the year. The first time the Fed attempted to shrink its balance sheet, the process was gradual, with caps on the amount of maturing securities (Treasuries and mortgage-backed securities) allowed to roll off each month.

The goal was to normalize monetary policy after the post-financial crisis quantitative easing (QE) programs, in an effort to move away from unconventional tools. Former Fed Chair Janet Yellen described the process as being "like watching paint dry," implying it was intended to be uneventful. The process ended abruptly after a sudden spike in short-term interest rates in September 2019. This indicated that bank reserves had dropped below the minimum level needed for the smooth functioning of funding markets, leading the Fed to stop QT and inject liquidity back into the system.

Our second attempt to implement quantitative tightening began in June 2022, which coincided with inflation spiking to more than 9% after money supply increased by approximately 40%. This was 10 years’ worth of money supply blasted into the economy in less than two years. As always, there are unintended consequences to such dramatic actions. The current round of QT is expected to end December 1, 2025. The pace of balance sheet reduction has been nearly double that of the 2017-2019 period.

The Fed's balance sheet has shrunk by over $2.5 trillion since its peak in April 2022 and now stands at approximately $6.5 trillion. The policy has contributed to generally higher interest rates and a reduction in the M2 money supply. The process has not been without complications; in March 2023, a "mini-crisis" occurred involving several U.S. banks that held large amounts of depreciated longer-duration Treasury bonds.

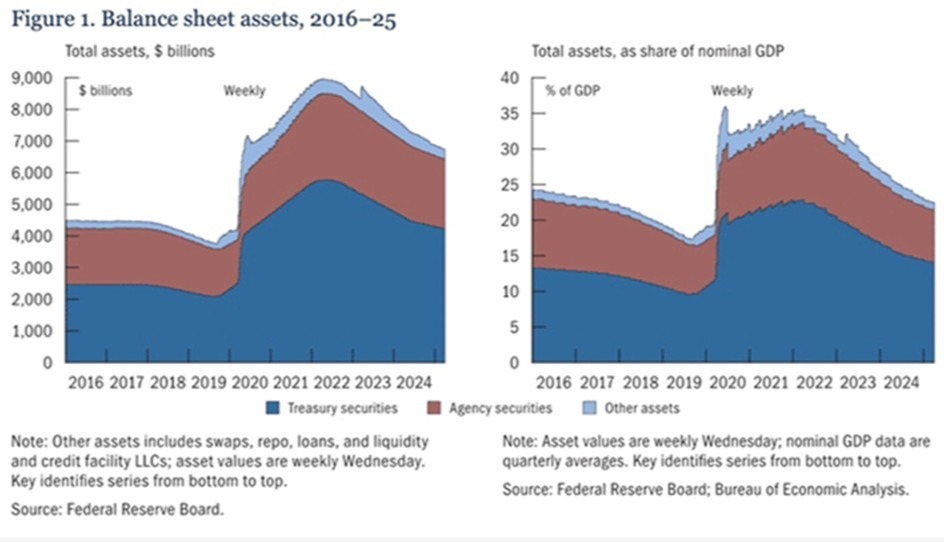

The Fed told us in October they will stop doing the “Tighten Up”. What are the implications of this? No one really knows the true minimum reserves necessary to keep markets stable. Jerome Powell has said the Fed wants to maintain a balance sheet “somewhat above the level consistent with ample reserves.” This means that the Fed wants a buffer and will likely stabilize the balance sheet near $5–6 trillion, not return to pre-2008 norms. That would put the new balance sheet floor at roughly 20% of GDP, or right around 2018 levels, as you can see on the right side of our final chart below. This would represent a permanent shift away from pre-GFC and COVID norms.

In summary, the Fed's experiences with QT have been challenging, with both episodes demonstrating the difficulty of smoothly withdrawing liquidity from the financial system without causing market volatility or instability. After more than three years of doing the “Tighten Up”, the Fed has decided to stop the dance. We will see what the outcome of their new policy stance will be. In the meantime, I wanted to keep you informed about these important, but often behind the scenes policy developments. It is part of my mission as we continue “Moving Life Forward.”

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/koya79