"Predictable" is the fourth track from the Kinks' 1981 album, Give the People What They Want. It was written by the group’s co-founder, Ray Davies. The song satirizes the conventional, unexciting life of the average person, a common theme in Ray's songwriting. As MTV launched in August 1981, this song and its quirky video played in heavy rotation in the early days of the station.

Source: Wikipedia & YouTube

The song is about the soul-crushing monotony and boredom of everyday middle-class life, with Ray Davies lamenting the lack of originality and the repetitive nature of existence, hoping for change but often feeling stuck in a cycle of routine, even contemplating that life's dullness makes death seem appealing. It's a sarcastic commentary on the mundane, where things happen "just like I've heard it all somewhere before.”

For those of you who are not familiar with the song or are too young to remember the early days of MTV (gasp), I have included a YouTube link to the often-played video below for your enjoyment and to give you a laugh about the early days of the music video.

The Kinks : Predictable (1981) *MTV*

Just as predictable as Ray Davies’ view of middle-class life, every December, Wall Street dusts off its crystal balls. Banks, strategists, and market commentators roll out their annual forecasts for the coming year — precise S&P 500 targets, carefully constructed narratives, and just enough confidence to suggest that this time they’ve finally figured it all out. It’s a ritual as dependable as the ball dropping in Times Square.

Davies sings about hoping for something different while quietly suspecting that nothing really ever is. Things happen “just like I’ve heard it all somewhere before.” If that doesn’t describe Wall Street’s annual market outlook season, it’s hard to imagine what does.

This year’s forecasts follow the same familiar script. According to Bloomberg, the average Wall Street strategist expects the S&P 500 to rise somewhere around 9–11% in 2026. Bloomberg tracks 21 major sell-side strategists, and this year, every single one of them is bullish. Not one is predicting a down year. One hundred percent bullish, as shown in our first chart below.

Source: TheStreet.com

That’s less a range of opinions and more a group consensus that borders on choreography. It feels reassuring, of course. There’s comfort in unanimity. But it’s worth remembering how often this particular movie ends badly. The Bloomberg article recently updated its annual strategist scorecard and found that, while forecasters were less wrong than usual last year, the longer-term record is still pretty grim. Before 2025, the consensus missed its year-end target by double digits eight years in a row. Eight. That’s not a rounding error — that’s a pattern.

To be fair, we’re asking strategists to do something close to impossible. Markets aren’t equations waiting to be solved. They’re living systems shaped by geopolitics, technological breakthroughs, policy decisions, investor psychology — and the occasional shock nobody had on their bingo card. Wars, elections, AI booms, AI disappointments, trade conflicts, fiscal missteps — none of these show up neatly in a twelve-month index target.

It’s even harder today because the market has become so top-heavy. A handful of mega-cap stocks now drive a disproportionate share of index returns. Forecasting where the S&P 500 will land requires very specific assumptions about a handful of tech/AI companies. That kind of granular company-level forecasting isn’t really what macro strategists are built to do — yet here we are, asking them to do it anyway.

And we keep doing it because the ritual itself feels useful. Clients ask for it. Media demands it. Having a forecast feels better than admitting uncertainty. Saying “here’s what we think will happen” is more comforting than saying “we don’t really know.”

Predictable.

Over the years, one lesson my mentors drilled into me was that when everybody is on the same side of the boat, it’s usually worth slowing down and reassessing. That doesn’t mean reflexively doing the opposite — it means recognizing when consensus starts to blur the line between confidence and complacency. Markets have a way of punishing consensus, especially when it drifts into complacency. Right now, if you define “everybody” as Wall Street analysts, they’ve been leaning the same way for a while — and they’re leaning even harder this year.

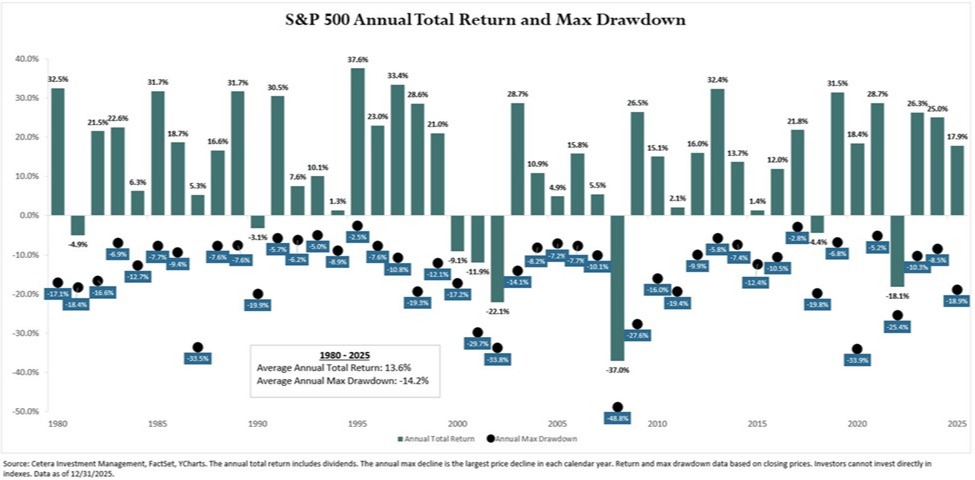

Historically, if you projected a higher S&P 500, you would have been right about 75% of the time since 1980. While this may sound reassuring at first glance, it leaves out some important context. The last time stocks rose for four or more consecutive years was 2003 through 2007. We all remember how that story ended. Even when markets finish higher, the path there is rarely smooth, and intra-year drawdowns have a nasty habit of shaking investors out at exactly the wrong moment, as shown in the chart below. Consensus forecasts never warn you about that part.

2025 turned out to be a pretty typical year for the stock market in comparison to the chart above. The S&P 500 finished with a 17.9% total return, despite an intra-year 18.9% correction. Volatility is common even in strong market years. Since 1980, the average intra-year drawdown is 14.2%, while the average annual return is 13.6%. To earn that average return, investors needed the intestinal fortitude to stay invested through those downturns. Human psychology, financial news channels, and social media make this exceedingly difficult.

This year’s outlooks span the usual extremes. On the bullish end, you have strategists pointing to steady earnings growth, supportive fiscal and monetary policy, and the continued spread of AI-driven investment as reasons the market could grind higher. Some of these voices have been right recently, which makes it tempting to believe they have a “hot hand.” On the bearish end, you have warnings about valuations, labor market cracks, and the possibility that the AI narrative doesn’t live up to its sky-high expectations. Those voices are often early, and sometimes wrong — until suddenly they aren’t.

That’s not a criticism of either camp. It’s a reminder that precision in markets is largely an illusion. The more confident and exact a forecast sounds, the more skeptical you should probably be. Which brings us to the part that actually matters. The purpose of market forecasts isn’t pinpoint accuracy. Getting the direction right alone is hard enough. Reviewing different scenarios can be useful — at least mentally — because it forces us to think about risks, opportunities, and what might go wrong as well as what might go right.

Your investment portfolio shouldn’t change simply because Analyst A is bullish or Strategist B is bearish. Portfolios are built for time horizons measured in years and decades, not calendar pages. They’re designed to survive uncertainty, not predict it away. What's most important to remember is that your age and risk-appropriate asset allocation portfolio is designed not to beat some prediction or index; it is designed to help you and your family reach their financial goals.

Ray Davies and the Kinks weren’t really singing about boredom. He was singing about the false comfort of routine — the idea that repetition equals safety, and that familiarity somehow grants control. Wall Street’s forecasting ritual does the same thing every year. It feels authoritative. It feels reassuring. It feels like someone, somewhere, has a handle on what comes next.

Markets, of course, have never been predictable. In hindsight, the years that matter most are usually the ones nobody sees coming.

If the consensus is right, 2026 will be a quiet, uneventful year. History suggests those are exactly the years markets refuse to deliver. That doesn’t feel like a great setup for boredom. This was another important lesson I wanted to share with you as we continue “Moving Life Forward.”

© 2026 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

The performance of any index is not indicative of the performance of any investment and does not indicative of the performance of investment and does not take into account the effects of inflation and the fees and expenses associated with the investing.

Featured Blog Image Source: iStock.com/natatravel