There was a time — and if you’re of a certain vintage, you can still hear it — when the most important debate in America wasn’t about inflation or interest rates. It was about beer.

Dim barroom lighting. Wood-paneled walls. A table full of oversized personalities arguing as if the fate of the republic depended on it. Billy Martin jabbing a finger. George Steinbrenner scowling. Dick Butkus leaning forward like it was fourth-and-goal. Bob Uecker wisecracking from somewhere near the cheap seats.

“Tastes Great!” “Less Filling!”

Back and forth. Loud. Passionate. Utterly convinced the other side was missing something obvious.

Source: YouTube

The brilliance of those old Miller Lite commercials wasn’t just the cast of sports icons selling what had once been considered a “diet” beer. It was the exposure of a false choice. The entire argument was built on the idea that you had to sacrifice one virtue to gain another.

Except you didn’t…You could have both.

If you are too young to remember these commercials or would simply like a chuckle from an earlier, simpler time, I have included a YouTube link to one of the classic Billy Martin/George Steinbrenner commercials.

Miller Lite Commercial (Martin & Steinbrenner, 1978)

For years, investors have lived inside their own version of that barroom shouting match.

“Higher Quality!” “Deeper Value!”

One camp insists you should own the highest-quality businesses…durable franchises, strong balance sheets, high returns on capital, steady earnings growth. The other camp demands a margin of safety…low price-to-earnings ratios, discounted price-to-book values, generous dividend yields. And for much of market history, it felt like you really did have to choose.

Quality stocks have historically traded at a premium. If you wanted consistent profitability and stable earnings, you paid up for it. You accepted lower dividend yields because great businesses reinvested for growth. You got the “tastes great” of high return on equity, but it cost you.

Value stocks, meanwhile, were the bargain aisle. Lower multiples. Higher yields. Slower growth. More cyclicality. Sometimes you find a reliable “used car” that does exactly what it promised. Other times, you found a value trap…a stock that looked cheap because the business model was quietly deteriorating.

For years, Wall Street has argued about this with the same theatrical conviction as those Miller Lite ads. Investors pounding tables on CNBC instead of bar tops. Factor models replacing football jerseys. But the tone? Not all that different.

What’s interesting right now is that the debate may be built on outdated assumptions.

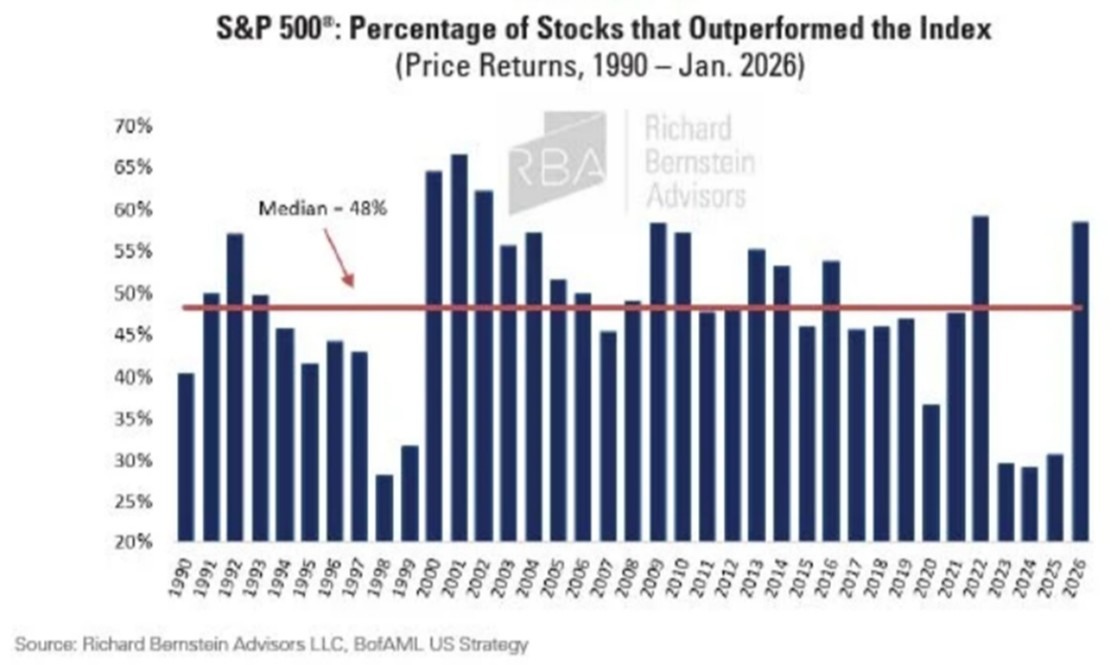

By the end of 2025, fewer stocks were beating the index than at any point since the late-1990s Tech Bubble.

Our first chart shows the percentage of S&P 500® stocks that outperformed the market by year. The period from 2023 to 2025 was the longest stretch of narrow leadership in the chart’s history.

One might think that an extreme market for so long might lead to unusual valuations and interesting investment opportunities, and it has. Leadership has finally begun to broaden in 2026.

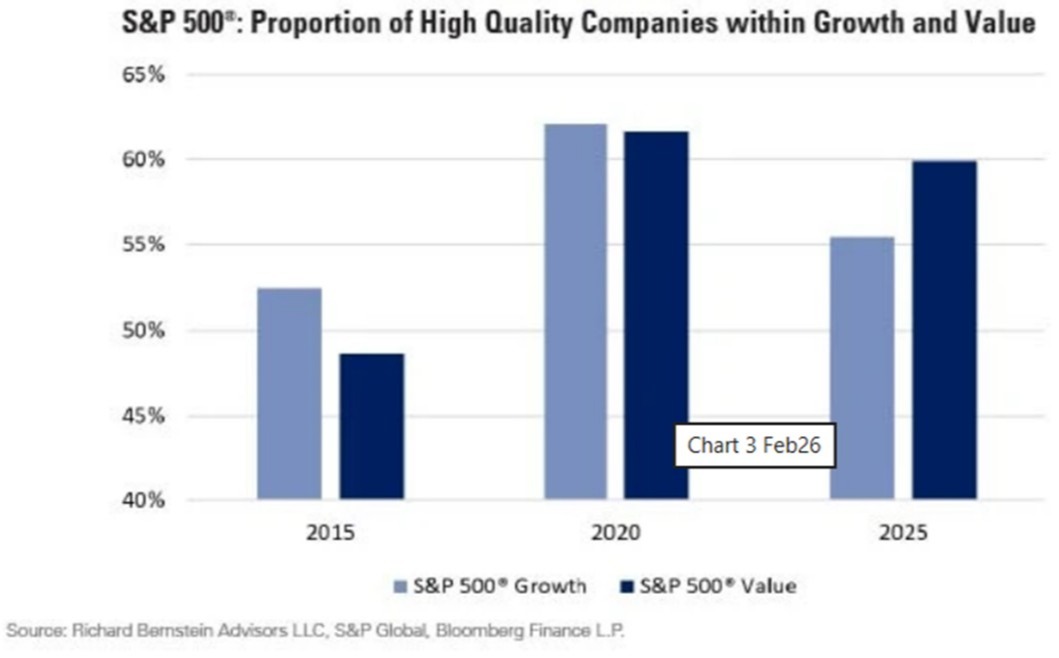

In several areas of today’s market, high-quality companies are trading at valuations that look far more like value stocks, as shown in our next chart below.

At the same time, many are offering dividend yields that are competitive with, or higher than, parts of the traditional value universe. That combination is not typical.

When Wall Street firms define “quality,” they do it systematically. They score companies on three core pillars: profitability, financial leverage, and earnings stability.

Profitability is often measured by Return on Equity, which reflects how effectively management turns shareholder capital into profit. Quality companies consistently generate strong ROE.

Financial leverage is typically captured through debt-to-equity ratios. Strong businesses don’t rely excessively on borrowed money. They have flexibility when credit conditions tighten.

Earnings stability looks at how predictable profits are over time. Durable companies produce recurring results rather than volatile spikes.

Put simply:quality companies make good money, don’t drown in debt, and don’t surprise you in unpleasant ways very often.

Value investing, by contrast, focuses on price. Major firms screen for low forward price-to-earnings ratios, low price-to-book values, attractive enterprise value relative to cash flow, and often higher-than-average dividend yields. They frequently apply sector-neutral approaches to avoid simply overweighting industries that are perpetually “cheap.”

The discipline exists for a reason. Not every low multiple represents opportunity. A stock can be inexpensive because it is misunderstood…or because it is structurally impaired. That’s the value trap investors rightly fear.

Historically, quality demanded a premium. That was rational. Investors were willing to pay more for stability, a strong balance sheet, and consistent execution. There are long stretches in market history when that premium widens considerably. That’s normal. That’s the cost of predictability.

What’s unusual is when the premium shrinks while the fundamentals don’t.

Over the last few years, higher interest rates reset valuation math across the market. When capital is no longer free, investors scrutinize balance sheets more closely. Cash flow matters more. Debt levels matter more. The speculative excesses that thrived in a zero-rate world lost some of their shine.

But valuation compression didn’t only hit the most speculative corners of the market. In many cases, it swept broadly, including companies that still exhibit strong profitability, manageable leverage, and stable earnings profiles.

The result? In certain sectors, you can now find companies that screen well on quality metrics and trade at forward multiples near or even below the broader market. Some are offering dividend yields that look far more “value” than “growth.”

You don’t often get that setup.

You’re not necessarily paying a luxury price for financial strength. You’re not forced to sacrifice balance sheet quality to generate income. You don’t have to accept fragile business models just to buy a lower multiple.

At Impel Wealth Management, we can focus on companies that generate strong returns on equity, carry reasonable debt, and produce consistent earnings, without paying a historic premium, as we manage portfolios for our friends and clients.

That doesn’t eliminate risk. It doesn’t mean every quality stock is suddenly a bargain. And it certainly doesn’t replace the disciplined analysis we strive to apply. But it does mean the trade-off isn’t as severe as it once was.

The chant was fun in a stadium. It’s less useful in portfolio construction.

Markets move in cycles. Factors rotate in and out of favor. There will come a time again when quality becomes scarce and expensive, or when bargains are plentiful, but balance sheets are shaky.

For now, though, the old argument feels a bit like that barroom debate.

“Tastes Great!” “Less Filling!”

Source: YouTube

The volume is high. The conviction is real.

But if you look closely at today’s valuations and fundamentals, you may find that you don’t actually have to choose.

And in investing — as in beer commercials — those moments don’t come around very often. I thought this was a fun way to share an important message as we continue “Moving Life Forward.”

© 2026 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/Davyd Kopych