"When I'm Sixty-Four" is a song by the English rock band The Beatles. It was written by Paul McCartney and credited to Lennon–McCartney. It was released on the 1967 album Sgt. Pepper's Lonely Hearts Club Band. In a 1987 interview he recalled, "Rock and Roll was about to happen that year, it was about to break, [so] I was still a little bit cabaret minded"

Source: YouTube

The song is sung by a young man to his girlfriend about his plans to grow old together. Although the theme is aging, it was one of the first songs McCartney wrote, at age 14, probably in April or May 1956. The song was recorded in a different key than the final version, sped up at McCartney's request to make his voice sound younger. It is also the only Beatles song that prominently features a trio of clarinets throughout.

"When I'm Sixty-Four" was included in the Beatles' 1968 animated film Yellow Submarine. Below is a YouTube link to that video.

The Beatles - When I'm Sixty Four (Official Video)

While the song above featured an average the age of 64, the average age for retirement in the United States is 62. Each year, I have a handful of clients who reach this critical age when they are contemplating retirement and becoming eligible for Social Security.

Clients turning 62 this year were born in 1963. Tying this back to our song above, this is the year Beatlemania broke out in Britain (It took another year for this phenomenon to reach America), Dr. Michael DeBakey performed the first human heart transplant, the Boston Celtics won their sixth NBA championship in seven years, and President John F. Kennedy was assassinated.

To put this in the perspective of the stock market, we ask the following three questions:

• Where did the S&P 500 close out 2024 relative to where it ended in 1963?

• Critically important to our clients planning on collecting dividends from their portfolio as part of their retirement income strategy: How much did the S&P 500 pay in cash dividends last year versus 1963?

• How did both price performance and dividend payments compare to consumer inflation—which will likely cause prices to double over a three-decade retirement?

And the answers:

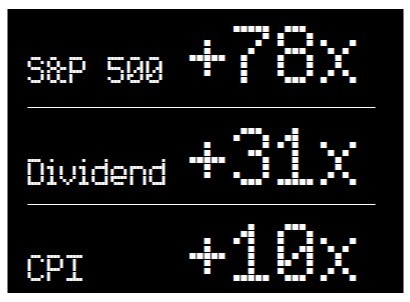

• The S&P 500 closed out 1963 at 75. It ended 2024 at 5,881.

• The cash dividend paid out in 1963 was $2.35. In 2024 it was $73.40.

• The Consumer Price Index ended 1963 at 31. It closed out 2024 at 318.

This means the S&P 500’s 62-year scorecard is as follows:

Source: Nick Murray Interactive

This means that over the first 62 years of our soon-to-be-retired clients’ lifetimes, the stock market has been the simplest and most effortless way of building real (net of inflation) wealth while generating dividend income in retirement that grows at a significant premium to the inflation rate.

However, there is only one way for you, our trusted friends and clients, to get these benefits throughout your investing lifetime: You have to stay invested. I could easily tick off any number of financial crises or market downturns that would have scared most people out of their well-planned investment portfolios over this 62-year time frame.

These would include three stock market downturns that nearly cut the index's value in half. We can start with the 73-74 inflation scare and Arab oil embargo, then move on to the dot.com bubble and 9/11, and finish with the events surrounding the 2008 financial crisis, culminating in the failure of AIG and Lehman Brothers.

I could add several dozen other minor crises that caused markets to drop by double digits. Each was accompanied by a media screaming that the sky was falling and the end of the world was coming… yet again. Each would have been enough to scare the average investor enough to cause them to lose faith and stop the compounding.

But YOU are not the average investor. You have a team of advisors at Impel Wealth Management who are here to support and shepherd you through the inevitable market ups and downs. You are also armed with the information and the wisdom that comes from the scorecard above.

Paul McCartney and The Beatles sang, “they would still need you and they would still feed you, when I’m 64.” However, we are much more concerned about our clients approaching retirement as early as age 62. We thought this was a great lesson and a fun way of sharing it with you as we continue “Moving Life Forward.”

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing.

Featured Blog Image Source: iStock.com/Jfanchin