Source: YouTube

When MTV first launched on August 1, 1981, I was watching. I was starting my sophomore year of high school, and with my love of music, I thought it was incredible to have a TV station completely dedicated to music videos. During those early days of programming, MTV had fewer than 200 videos in its library. The first day alone featured 116 unique videos played, spanning 209 total spins. MTV utilized a rotation system, repeating videos throughout the day to fill the 24-hour programming.

The playlist from the first day is available online. For those of you who are music history enthusiasts or simply love 70s and 80s music, I encourage you to search the list for some of your favorites. Artists who played in heavy rotation during these early days of MTV included Rod Stewart, David Bowie, The Pretenders, Pat Benatar, The Ramones, The Who, Elvis Costello, The Specials, Split Enz, and REO Speedwagon, who, by my count, appeared 15 separate times in the first 24 hours of the new network.

Source Wikipedia

REO Speedwagon has sold more than 40 million records and charted 13 Top 40 hits, including the number ones "Keep on Loving You" and "Can't Fight This Feeling". You Can Tune a Piano, but You Can't Tuna Fish was REO Speedwagon's seventh studio album, released in 1978. The album opens with the song "Roll with the Changes," which played in heavy rotation in the early days of MTV. Cash Box said that it "opens with a flowing piano riff that quickly develops into a dynamic, well-structured tune propelled by electrifying guitar licks." For those of you who do not remember this early MTV song, or who want a reminder, a link to the YouTube video of a live version of the song is included below.

Source: Discogs

REO Speedwagon - Roll with the Changes (Color Version)

It is very apparent to everyone, other than those on Capitol Hill, that Social Security needs to “Roll with the Changes” as well, if it is going to stay solvent long term and remain a pillar of most seniors' retirement income plans. This was made evident in the 2024 Social Security Trustees Report, which was released on May 6, 2024. This report provides an annual assessment of the long-term financial status of the Social Security system. It indicated that Social Security's trust funds will be unable to pay full benefits beginning in 2035.

The report's conclusion states the obvious and calls for lawmakers to address this situation sooner rather than later so that whatever changes are adopted can be phased in and implemented in a less draconian manner. I fully agree with this and have been writing about and calling for these changes for nearly 20 years.

CONCLUSION

The 2024 Trustees Reports indicate a need for substantial changes to address Social Security’s and Medicare’s financial challenges. The Trustees recommend that lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust their expectations and behavior. Implementing changes sooner rather than later would allow more generations to share in the needed revenue increases or reductions in scheduled benefits. With informed discussion, creative thinking, and timely legislative action, Social Security and Medicare can continue to protect future generations.

Senate procedural rules prevent using the budget reconciliation process to change Social Security. The Congressional Budget Act of 1974, which introduced budget reconciliation, explicitly prevents changes to Social Security unless normal rules are followed. Since it’s unlikely that a party will control at least 60 seats in the Senate, making significant changes will require bipartisan support. As the new administration explores options to reduce federal government spending, concerns around modifications to Social Security are rising. For example, what actions may be considered that could potentially impact Social Security benefits? There have been discussions about closing offices or reducing the workforce of the Social Security Administration. These changes could reduce administrative costs, leaving more money for future benefits. However, making structural modifications to Social Security, such as raising the retirement age, is more complicated. For this reason, major changes to Social Security in the near term are unlikely.

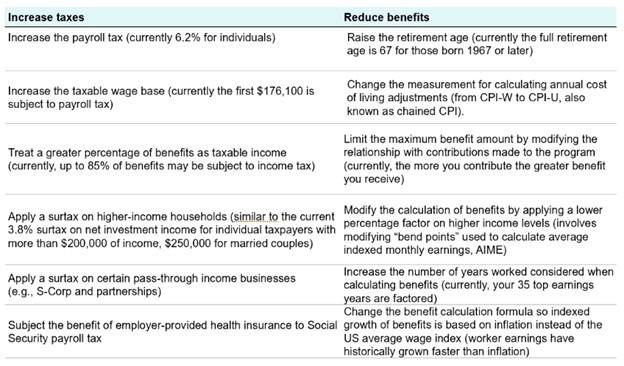

As I have stated many times before, fixing Social Security is not that difficult. It is simply a matter of math. Many levers can be pulled to raise revenue or reduce benefits. These levers must be pulled in some combination to create a formula that makes Social Security sustainable for future generations. Our friends at Franklin Templeton have compiled a list of potential policy options to fix Social Security. I have included a copy of the options in chart form below.

Source: Advisor Perspectives Franklin Templeton

Some of the most talked-about options include increasing the FICA payroll tax, which is currently 6.2%, for all employees, or raising the age for full retirement benefits from 67 to 69 or 70 for people under age 40. There is also talk of increasing the taxable wage base on which people pay Social Security tax. Currently, employment earnings below $176,100 are subject to the Social Security payroll tax. Originally, the taxable wage base was designed to cover 90% of earnings in the United States. Currently, 83% of earnings are subject to Social Security payroll tax since wages for higher-income taxpayers have grown faster than those of lower-income taxpayers. If policymakers wanted to reach the 90% target now, the taxable wage base would have to increase to roughly $300,000.

The long-term future of Social Security is in the balance. However, even if Congress doesn’t act, beneficiaries are projected to receive roughly 80% of scheduled benefits. There is confusion that the depletion of the trust fund will mean that benefits are completely gone. This is not the case. However, prudent planning must incorporate the risks of a reduced benefit amount in the future, higher taxes, or both. For those nearing retirement in the next decade, it would be prudent to approach claiming Social Security benefits thoughtfully, especially if those benefits are the only source of guaranteed, lifetime income. Avoid making a rash decision to claim Social Security early just because you’ve heard the trust fund is being exhausted. An eventual plan to address the issue will likely not impact current and near retirees as much as younger workers.

I firmly believe that the number one goal of any lawmaker, Democrat or Republican, once elected, is to get reelected. One of the best ways to not get reelected is to jeopardize a retirement income pillar that more than 70 million Americans rely on. This is why I am confident this will be addressed...eventually. However, as is typical, Congress will kick the can down the road as long as possible, until they are forced to “Roll with the Changes.” The CFPs of Impel Wealth Management will do our best to keep you informed about this critical topic as we continue “Moving Life Forward.”

© 2025 Jesse Hurst

Senior Wealth Manager

Related Content

The views stated are not necessarily the opinion of Cetera and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Neither Cetera Advisors LLC nor any of its representatives may give legal or tax advice. This information is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Investors cannot directly invest in indices.

Featured Blog Image Source: iStock.com/useng